Legal Deed in Lieu of Foreclosure Form for Georgia

In Georgia, homeowners facing the possibility of foreclosure have an alternative option to navigate their financial distress. The Deed in Lieu of Foreclosure form stands as a critical document in this process, offering a voluntary transfer of property ownership from the borrower to the lender. This legal arrangement serves to satisfy the outstanding debt on the mortgage, often sparing both parties the time, expense, and stress associated with foreclosure proceedings. It is a mutually beneficial solution that hinges on agreement from both the lender and the borrower. Importantly, this form encompasses several vital components that need careful consideration, including the full legal description of the property, the terms of the agreement between the borrower and the lender, and any additional conditions that must be met. Proper execution of this document requires a thorough understanding of its content and implications, making it essential for homeowners to seek comprehensive advice and ensure all parties are fully informed before proceeding.

Form Sample

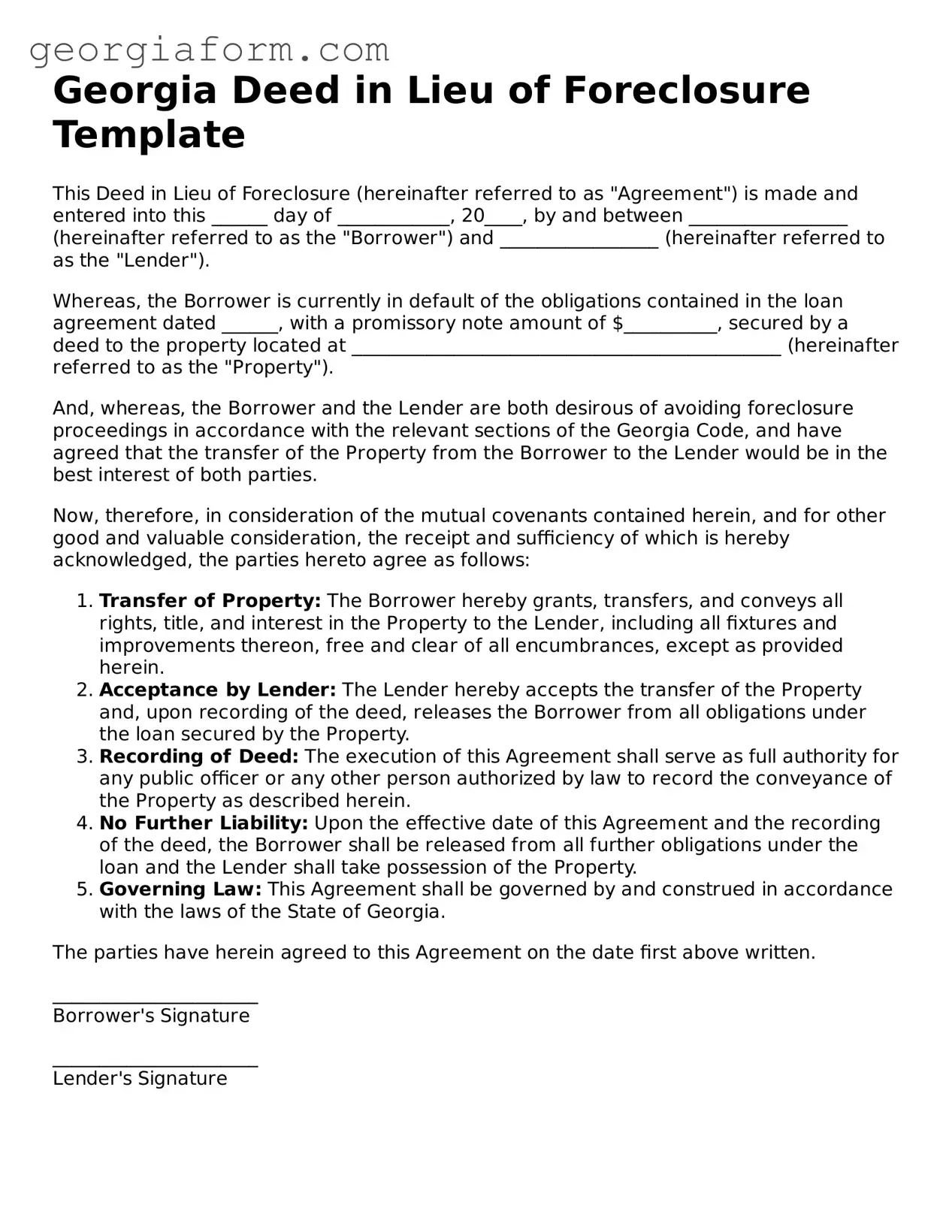

Georgia Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure (hereinafter referred to as "Agreement") is made and entered into this ______ day of ____________, 20____, by and between _________________ (hereinafter referred to as the "Borrower") and _________________ (hereinafter referred to as the "Lender").

Whereas, the Borrower is currently in default of the obligations contained in the loan agreement dated ______, with a promissory note amount of $__________, secured by a deed to the property located at ______________________________________________ (hereinafter referred to as the "Property").

And, whereas, the Borrower and the Lender are both desirous of avoiding foreclosure proceedings in accordance with the relevant sections of the Georgia Code, and have agreed that the transfer of the Property from the Borrower to the Lender would be in the best interest of both parties.

Now, therefore, in consideration of the mutual covenants contained herein, and for other good and valuable consideration, the receipt and sufficiency of which is hereby acknowledged, the parties hereto agree as follows:

- Transfer of Property: The Borrower hereby grants, transfers, and conveys all rights, title, and interest in the Property to the Lender, including all fixtures and improvements thereon, free and clear of all encumbrances, except as provided herein.

- Acceptance by Lender: The Lender hereby accepts the transfer of the Property and, upon recording of the deed, releases the Borrower from all obligations under the loan secured by the Property.

- Recording of Deed: The execution of this Agreement shall serve as full authority for any public officer or any other person authorized by law to record the conveyance of the Property as described herein.

- No Further Liability: Upon the effective date of this Agreement and the recording of the deed, the Borrower shall be released from all further obligations under the loan and the Lender shall take possession of the Property.

- Governing Law: This Agreement shall be governed by and construed in accordance with the laws of the State of Georgia.

The parties have herein agreed to this Agreement on the date first above written.

______________________

Borrower's Signature

______________________

Lender's Signature

PDF Data

| Fact Number | Description |

|---|---|

| 1 | The Georgia Deed in Lieu of Foreclosure is a legal document used by a borrower to convey real property ownership back to the lender to avoid foreclosure. |

| 2 | This form effectively transfers the property's title from the homeowner to the bank or mortgage company holding the mortgage. |

| 3 | It serves as an alternative to foreclosure proceedings, which can be lengthy, costly, and damage the borrower's credit. |

| 4 | The deed in lieu of foreclosure must be agreed upon by both the lender and the borrower, indicating a cooperative approach to the situation. |

| 5 | Under Georgia law, particularly the Georgia Code, the process and requirements for deeds in lieu of foreclosure are outlined, ensuring all parties understand their rights and obligations. |

| 6 | Parties may incorporate a deficiency waiver into the agreement, which means the lender forgives any balance owed by the borrower after the property's transfer. |

| 7 | Completion and recording of the deed in lieu of foreclosure in the county where the property is located is necessary to make the transfer effective and public. |

| 8 | Tax implications for the borrower could arise from a deed in lieu of foreclosure, given that the forgiven debt may be considered taxable income under certain circumstances. |

| 9 | Before proceeding, homeowners are advised to consult with legal and tax professionals to fully understand the benefits and potential drawbacks of using a deed in lieu of foreclosure in Georgia. |

Guide to Using Georgia Deed in Lieu of Foreclosure

Filling out the Georgia Deed in Lieu of Foreclosure form is a crucial step for homeowners wishing to avoid the foreclosure process by voluntarily transferring their property title to the lender. This process offers a way to address an outstanding mortgage under mutually agreed terms between the borrower and the lender, which can minimize damage to the borrower's credit score compared to a foreclosure. Following the correct steps is essential for a smooth transaction and to ensure all legal requirements are met. Bear in mind, this is a general guide, and it is highly recommended to seek legal advice or assistance to navigate through this process accurately.

- Gather all necessary information including the property description, current mortgage details, and both the lender's and borrower's contact information.

- Start by entering the date at the top of the form.

- Fill in the borrower's full legal name(s) as the "Grantor(s)," making sure it matches the name on the property title and mortgage documents.

- Enter the legal name of the lender (or their authorized representative) as the "Grantee."

- Provide a complete legal description of the property. This information can be found on your original mortgage documents or by contacting your local county recorder's office.

- Specify the amount of outstanding debt this deed in lieu is settling. If not specified, refer to the agreement made with the lender.

- Include any additional agreements made between the borrower and lender regarding the property transfer. This may include terms about debt forgiveness, any remaining debt obligations, or conditions that must be met before the transfer takes effect.

- Both the borrower and the lender must sign and date the form in the presence of a notary public to acknowledge the voluntary transfer of property.

- Ensure the form is notarized. The notary will fill in their section, certifying that both parties signed the document in their presence.

- File the completed form with the county recorder's office where the property is located to make the transfer official.

- Keep a copy of the filed form for your records.

Once the form is properly filled out and filed, the property's title is officially transferred to the lender, thereby avoiding the formal foreclosure process. It's important to verify that the transfer has been recorded correctly by checking with the county recorder's office. Remember, this process does not automatically relieve the borrower from all financial obligations associated with the mortgage. Any remaining debts or impacts on the borrower’s credit score should be discussed and fully understood before finalizing a deed in lieu of foreclosure.

Obtain Clarifications on Georgia Deed in Lieu of Foreclosure

-

What is a Deed in Lieu of Foreclosure in Georgia?

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to transfer the ownership of their property back to the lender voluntarily. This action is taken to avoid the process of foreclosure. In Georgia, this serves as an alternative for homeowners who are unable to continue making payments on their mortgages, offering a way to prevent the lengthy and costly procedure of foreclosure.

-

How does a Deed in Lieu of Foreclosure work in Georgia?

In this process, the homeowner and the lender must agree that the deed to the property will be transferred to the lender. The agreement effectively cancels the borrower's mortgage debt. Often, but not always, the lender may also agree to forgive any deficiency balance - the difference between the sale price of the property and the mortgage balance. However, the terms are subject to negotiation between the borrower and the lender.

-

What are the benefits of a Deed in Lieu of Foreclosure for homeowners?

It can help avoid the negative impact of a foreclosure on the homeowner's credit report.

It might release the homeowner from the obligation to repay the mortgage balance, if agreed upon with the lender.

It can provide a more dignified exit from the property compared to the foreclosure process.

-

Are there any drawbacks to a Deed in Lieu of Foreclosure for Georgia homeowners?

It may still negatively affect the homeowner's credit score, though typically less than a foreclosure would.

Not all lenders will agree to a Deed in Lieu of Foreclosure, especially if there are other liens on the property.

The homeowner may still be responsible for the deficiency balance unless explicitly forgiven in the agreement.

-

How can a homeowner request a Deed in Lieu of Foreclosure in Georgia?

The first step is contacting the lender to discuss the possible hardships that make it difficult for the homeowner to continue paying the mortgage. The lender may then provide the homeowner with a Deed in Lieu of Foreclosure form or tell them how to obtain one. It's crucial for homeowners to get everything in writing and, if possible, consult with an attorney specializing in real estate before proceeding.

-

Is it necessary to have a lawyer to complete a Deed in Lieu of Foreclosure in Georgia?

While it's not mandatory to have a lawyer, it's highly recommended. A lawyer can help negotiate the terms with the lender, ensuring the homeowner's rights are protected and providing advice on how the Deed in Lieu of Foreclosure might affect their future financial situation. Legal representation can also clarify the potential tax implications of the deal.

Common mistakes

-

Not consulting with a legal or financial advisor before proceeding. This step is crucial as it helps understand the implications of a Deed in Lieu of Foreclosure.

-

Failure to verify that all parties are in agreement with the terms before submitting the form. Without the consent of all involved parties, the deed might not be legally binding.

-

Omitting necessary details about the property, such as its full address and any identifying lot or parcel numbers. This information is critical for accurately identifying the property in legal documents.

-

Leaving out important personal information, including the full legal names and contact details of the borrower and lender. Accurate information is essential for the validity of the document.

-

Neglecting to attach all required documents, such as proof of financial hardship or any agreement related to the deed. These documents provide context and support for the transaction.

-

Signing the document without having it notarized. In Georgia, notarization is a legal requirement for a Deed in Lieu of Foreclosure to be considered valid.

-

Ignoring potential tax implications or not seeking advice on how to handle them. A Deed in Lieu of Foreclosure can have significant tax consequences for the homeowner.

-

Failing to confirm that the mortgage company agrees not to pursue a deficiency judgment. Without this assurance, homeowners might still be liable for the difference between the sale price and the mortgage balance.

-

Misunderstanding the legal implications, such as assuming that the deed clears all debts related to the property. It's important to know exactly what responsibilities remain post-deed.

-

Submitting the form without keeping a copy for personal records. It is vital to have proof of submission and a personal copy for future reference.

By avoiding these mistakes, homeowners can ensure a smoother process while navigating through the complexities of a Deed in Lieu of Foreclosure.

Documents used along the form

When dealing with the complexities of avoiding foreclosure, property owners in Georgia might consider a Deed in Lieu of Foreclosure as a viable option. This form is critical in enabling homeowners to voluntarily transfer property ownership back to the lender as an alternative to foreclosure. Yet, completing this process requires more than just the Deed in Lieu of Foreclosure form. Several other documents are typically involved, each serving a distinct purpose in ensuring the transaction is legally sound and comprehensive. Understanding these documents is essential for a smooth transition.

- Promissory Note: This is a vital document that outlines the borrower's promise to repay the loan. It includes details such as the loan amount, interest rate, payment schedule, and maturity date. When entering a deed in lieu of foreclosure, the promissory note helps determine the remaining debt obligation, if any, after the property's transfer.

- Hardship Letter: The property owner must provide a hardship letter explaining the circumstances that have led to their financial difficulties. This document should convincingly demonstrate why the homeowner is unable to continue making mortgage payments, making the case for why a deed in lieu of foreclosure is necessary.

- Property Appraisal Report: An appraisal of the property is typically required to establish its current market value. This ensures that the lender is making an informed decision based on the property's worth. It also influences the negotiation regarding any deficiency balance that might remain after the deed in lieu process is complete.

- Settlement Statement: This document provides a comprehensive breakdown of the transaction, including any remaining mortgage balance, potential fees, and adjustments. A settlement statement is crucial for clarity, ensuring both parties agree on the terms and understand the financial implications of the deed in lieu of foreclosure.

Equipped with these documents, homeowners and lenders can proceed with confidence, knowing they have considered all legal and financial aspects of the deed in lieu of foreclosure process. Each document serves a specific purpose, contributing to the transparency and fairness of the transaction. For anyone navigating this path, it's advised to seek legal counsel to ensure all paperwork is handled correctly and deadlines are met, thereby avoiding common pitfalls and streamlining the process towards a satisfactory resolution.

Similar forms

Mortgage Agreement: Just like a Deed in Lieu of Foreclosure form, a Mortgage Agreement is a crucial document in real estate transactions. It outlines the loan terms for purchasing property. Both documents are involved in the financing and ownership aspects of real estate, but while a Mortgage Agreement initiates the loan process, a Deed in Lieu of Foreclosure concludes it by transferring property ownership back to the lender to avoid foreclosure.

Loan Modification Agreement: This document is similar because it also relates to adjusting the terms of an existing mortgage, aimed at preventing foreclosure. A Deed in Lieu of Foreclosure and a Loan Modification Agreement are both tools for homeowners struggling with mortgage payments, offering alternatives to losing their homes.

Short Sale Approval Letter: This letter from a lender authorizes the sale of a property for an amount less than the mortgage owed. Both the Deed in Lieu of Foreclosure and the Short Sale Approval Letter are used when homeowners cannot afford their mortgage, offering a way out that can be less damaging to their credit than foreclosure.

Foreclosure Notice: This notice is a legal document that a lender sends to notify a borrower of the commencement of foreclosure proceedings. Foreclosure Notices and Deeds in Lieu of Foreclosure are closely related as they both deal with the outcome of defaulting on a mortgage, but a Deed in Lieu is a voluntary transfer to avoid the full foreclosure process.

Quit Claim Deed: Used to transfer any interest in real property without making any guarantees about the title, Quit Claim Deeds share similarities with Deeds in Lieu of Foreclosure in that they are both methods of transferring property rights. However, the contexts differ greatly, with Deeds in Lieu being a specific tool to avoid foreclosure.

Bankruptcy Discharge Papers: After successfully completing a bankruptcy process, these papers officially release a debtor from certain debts. Although dealing with different aspects of financial distress, both Bankruptcy Discharge Papers and Deeds in Lieu of Foreclosure represent ways individuals can manage overwhelming debt, specifically regarding home ownership and mortgages.

Dos and Don'ts

When filling out the Georgia Deed in Lieu of Foreclosure form, certain practices should be followed to ensure the process is completed accurately and effectively. Paying attention to these dos and don'ts can help you avoid common pitfalls and make the transaction smoother for all parties involved.

Do:

- Review the original loan agreement and any other related documents to ensure that a deed in lieu of foreclosure is permitted under the terms and to understand any prerequisites or specific requirements.

- Ensure that all parties to the deed (the borrower(s) and the lender or its representative) have their details correctly filled out, including full legal names and contact information.

- Clearly describe the property being transferred, including the legal description as found in the current deed or property tax documents to avoid any ambiguity about the property in question.

- Ensure that any and all liens or encumbrances on the property are disclosed to and acknowledged by the lender before finalizing the deed in lieu of foreclosure, as they may impact the lender's willingness to accept the deed.

- Check with local authorities or a legal advisor to see if any additional forms or steps are required in your county for a deed in lieu of foreclosure to be recognized and effective.

Don't:

- Attempt to hide any property defects or financial issues related to the property from the lender. Full disclosure is key in the process of a deed in lieu of foreclosure, and failing to disclose information may lead to legal consequences.

- Sign the deed in lieu of foreclosure document without ensuring that all debt obligations will be satisfied, or clearly understanding if any financial obligations will remain after the transfer of property.

- Proceed without legal advice if you are unsure about any part of the process or the ramifications of a deed in lieu of foreclosure. A legal advisor can provide clarity and guidance tailored to your specific situation.

- Forget to check if the lender requires the form to be notarized. In Georgia, deeds must typically be notarized to be recorded and considered valid.

- Complete the deed in lieu of foreclosure in haste. Take your time to fill out all sections accurately and review the document thoroughly before submission.

Misconceptions

When dealing with the Georgia Deed in Lieu of Foreclosure, several misconceptions can cloud a homeowner's understanding. It's important to distinguish fact from fiction to navigate this process effectively.

- It immediately clears all debt associated with the property. Many believe that by accepting a deed in lieu of foreclosure, they are freed from all their mortgage obligations. However, this is not always the case. If the property’s sale does not cover the total debt owed, the lender may still pursue a deficiency judgment, depending on the terms of the agreement and Georgia state laws.

- It has no impact on credit scores. Another common misconception is that a deed in lieu of foreclosure will not affect the homeowner's credit score. While it may have a less severe impact than a foreclosure, it still negatively affects the credit score. Lenders report it to credit bureaus as a settlement, which can lower scores and influence future borrowing capabilities.

- It’s an option for all homeowners facing foreclosure. Not all homeowners are eligible for a deed in lieu of foreclosure. Lenders typically require a thorough assessment of the homeowner's financial situation, and there must be a clear title. Additionally, if there are any secondary liens on the property, it might complicate approval.

- The process is quick and effortless. Some people might think that opting for a deed in lieu of foreclosure offers a fast and easy way out of their mortgage troubles. However, the process involves detailed negotiations with the lender, including the settlement of any remaining debt, and the transfer of the property’s title. This can be time-consuming and requires careful handling to ensure that all legal and financial responsibilities are addressed.

Key takeaways

Filling out and using the Georgia Deed in Lieu of Foreclosure form is a significant step for homeowners facing the prospect of foreclosure. It allows a borrower to transfer the ownership of the property back to the lender voluntarily. This process can be complex and sensitive, so understanding the key points is crucial for anyone considering this option. Here are some critical takeaways:

- Understand what it is: A Deed in Lieu of Foreclosure is a legal document where the homeowner voluntarily transfers the deed of the property back to the lender to avoid foreclosure.

- Assess all options: Before deciding on a deed in lieu of foreclosure, homeowners should consider all available foreclosure prevention options. Consulting with a financial advisor or attorney can provide valuable guidance.

- Communication with the lender is key: The process begins by contacting the lender to discuss the possibility of a deed in lieu of foreclosure. Open and honest communication is essential for a successful negotiation.

- Financial documents: Homeowners will need to provide comprehensive financial information to the lender. This includes, but is not limited to, proof of income, tax returns, and a hardship letter explaining why they cannot continue making mortgage payments.

- Understand the impact on credit: While a deed in lieu of foreclosure may have a less severe impact on a homeowner’s credit score than a foreclosure, it can still negatively affect credit. It is important to understand this impact fully.

- Release of deficiency rights: In the agreement, ensure that the lender agrees to forgive any deficiency balance - the difference between the sale proceeds and the amount owed on the mortgage - to avoid being responsible for any remaining debt.

- Seek legal advice: It is crucial to consult with an attorney who specializes in real estate or foreclosure law in Georgia to help navigate the complexities of the process and protect your interests.

- Eligibility criteria: Not all homeowners or properties are eligible for a deed in lieu of foreclosure. Lenders have specific criteria, which can include the absence of other liens or mortgages on the property.

- Understand tax implications: There can be tax consequences for a deed in lieu of foreclosure. Canceled or forgiven debt may be considered taxable income. Homeowners should consult with a tax advisor to understand their potential tax liability.

The decision to pursue a deed in lieu of foreclosure should not be taken lightly. Comprehensive understanding of the process, implications, and eligibility requirements is crucial. By considering these key takeaways, homeowners can make informed decisions best suited for their financial situation. Always remember, professional advice from attorneys and financial advisors is invaluable in these circumstances.

More Georgia Templates

How to Transfer a House Deed - In some cases, the use of a Gift Deed can facilitate a smoother probate process by clearly delineating what assets have been given away during the donor's lifetime.

Are Companies Required to Have an Employee Handbook - Advises on the proper use of company communication tools, emphasizing efficiency and etiquette in internal and external correspondence.