Free Georgia 600 T Template in PDF

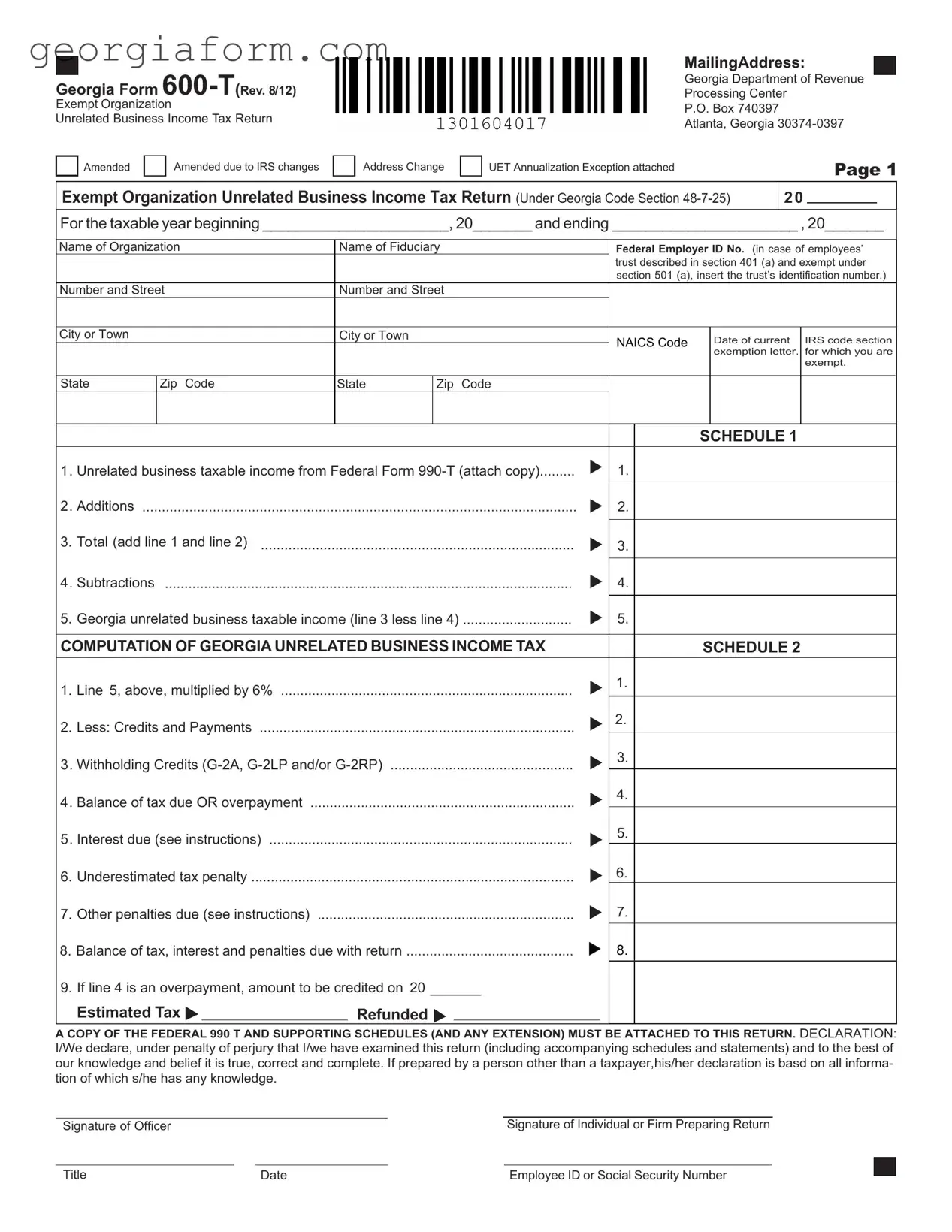

In the landscape of tax obligations for exempt organizations, the Georgia 600-T form plays a critical role. This form, officially known as the Exempt Organization Unrelated Business Income Tax Return, is devised under the Georgia Code Section 48-7-25, marking its significance for organizations that steer clear from profit motives yet engage in revenue-generating activities unrelated to their primary exempt purpose. Each year, organizations must meticulously report their unrelated business income, drawing upon the initial figures from the Federal Form 990-T and making necessary adjustments to mirror Georgia's tax code requirements. The form intricately details the computation of unrelated business income tax, embracing a fixed 6% rate, while also providing space for deductions, credits, and payments that could influence the final tax obligation. Moreover, it underscores the importance of adherence to filing deadlines, mirroring those of the federal counterpart, while allowing a leeway through extensions under reasonable circumstances. The accompanying instructions shed light on accounting methods, period coverage, and the intricacies of apportioning income and expenses, ensuring organizations can accurately reflect their Georgia taxable income. Delinquency in filing or payment triggers penalties and interest, emphasizing the need for punctuality and accuracy. Additionally, the mandate to attach a copy of the Federal 990-T underscores the interconnectedness of federal and state tax reporting obligations. This multi-faceted form is not just a tax document but a testament to the regulatory framework that balances the tax privileges of exempt organizations with their unrelated business income activities within Georgia.

Form Sample

Georgia Form

Exempt Organization

Unrelated Business Income Tax Return

Amended |

|

Amended due to IRS changes |

|

|

|

Address Change

MailingAddress:

Georgia Department of Revenue

Processing Center

P.O. Box 740397

Atlanta, Georgia

UET Annualization Exception attached |

PAGE 1 |

|

Exempt Organization Unrelated Business Income Tax Return (Under Georgia Code Section

20

For the taxable year beginning ______________________, 20_______ and ending ______________________ , 20_______

Name of Organization |

Name of Fiduciary |

|

Federal Employer ID No. (in case of employees’ |

||||

|

|

|

|

|

trust described in section 401 (a) and exempt under |

||

|

|

|

|

|

section 501 (a), insert the trust’s identification number.) |

||

Number and Street |

Number and Street |

|

|

|

|

||

|

|

|

|

|

|

|

|

City or Town |

|

City or Town |

|

|

NAICS Code |

Date of current |

IRS code section |

|

|

|

|

|

|||

|

|

|

|

|

|

exemption letter. |

for which you are |

|

|

|

|

|

|

|

exempt. |

|

|

|

|

|

|

|

|

State |

Zip Code |

State |

Zip |

Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SCHEDULE 1 |

|

1. Unrelated business taxable income from Federal Form |

1. |

||||||||

2. Additions |

|

|

|

|

|

|

|||

|

|

|

|

2. |

|||||

3. |

Total (add line 1 and line 2) |

|

|

|

|

|

|

||

|

|

|

|

3. |

|||||

4. Subtractions |

|

|

|

|

|

|

|||

|

|

|

|

4. |

|||||

5. |

Georgia unrelated business taxable income (line 3 less line 4) |

|

|||||||

5. |

|||||||||

|

|

|

|

|

|

|

|||

COMPUTATION OF GEORGIAUNRELATED BUSINESS INCOME TAX |

SCHEDULE 2 |

||||||||

1. |

Line 5, above, multiplied by 6% |

|

|

|

|

|

1. |

||

|

|

|

|

|

|||||

2. |

Less: Credits and Payments |

|

|

|

|

|

2. |

||

|

|

|

|

|

|||||

3. Withholding Credits |

3. |

||||||||

4. |

|||||||||

4. Balance of tax due OR overpayment |

|

|

|

|

|

||||

|

|

|

|

|

|||||

|

|

|

|

|

5. |

||||

5. Interest due (see instructions) |

|

|

|

|

|

||||

|

|

|

|

|

|||||

|

|

|

|

|

6. |

||||

6. |

Underestimated tax penalty |

|

|

|

|

|

|||

7. |

Other penalties due (see instructions) |

|

|

|

|

7. |

|||

8. Balance of tax, interest and penalties due with return |

8. |

||||||||

9. |

If line 4 is an overpayment, amount to be credited on 20 |

|

|

|

|||||

|

|||||||||

|

Estimated Tax |

|

Refunded |

|

|

|

|||

A COPY OF THE FEDERAL 990 T AND SUPPORTING SCHEDULES (AND ANY EXTENSION) MUST BE ATTACHED TO THIS RETURN. DECLARATION: I/We declare, under penalty of perjury that I/we have examined this return (including accompanying schedules and statements) and to the best of our knowledge and belief it is true, correct and complete. If prepared by a person other than a taxpayer,his/her declaration is basd on all informa- tion of which s/he has any knowledge.

Signature of Officer |

|

Signature of Individual or Firm Preparing Return |

Title |

Date |

Employee ID or Social Security Number |

PAGE 2

INSTRUCTIONS FOR FORM

FILING REQUIREMENTS

Everyexemptorganization,whichis requiredto filea Form

or business income from Georgia sources, must file a

Georgia Form

WHENAND WHERE TO FILE

The return is due on or before the due date of the Federal Form

EXTENSION OF TIME

A reasonableextensionof time for filing may be granted by the Commissioner upon application on Form

TAX RATE

As provided by Georgia Code Section

ACCOUNTING METHOD

Taxable income must be computed using the method of accountingregularlyusedinkeepingtheorganization’sbooks and records. In all cases, the method adopted must clearly reflect taxable income.

PERIOD TO BE COVERED

The taxable period for Georgia purposes shall be the same as for Federal purposes.

ALLOCATION AND APPORTIONMENT OF INCOMEAND EXPENSES

For those organizations having unrelated business income for Georgia and in other states, the income and expenses relatedtoitsproductionshouldbeallocatedandapportioned to clearly reflect the Georgia unrelated business taxable income. Sufficient information should be attached to the Form

PENALTIESAND INTEREST

Penalties provided by the Georgia Code are: For delin- quent filing- 5% of tax not paid by the original due date for each month or part of month of delinquency. For delinquent payment- 1/2 of 1% due for each month or part month of delinquency. An extension of time for filing does not alter delinquent payment penalty. Delin- quent payment is not due if the return is being amended due to an IRS audit. For negligent underpayment- 5% of amount of

Underpayment of estimated tax (UET) Penalty. Attach Form 600 UET and enter the amount on line 6. Also if a penalty exception applies check the “UET Annualization Exception attached” box.

NOTE:Thecombinedtotalofthepenaltyfordelinquentfiling and penalty for delinquent payment cannot exceed 25% of the tax not paid by the original due date.

FEDERAL FORM

“Georgia Public Revenue Code Section

File Overview

| Fact Name | Description |

|---|---|

| Form Designation | Georgia Form 600-T is designated as the Exempt Organization Unrelated Business Income Tax Return. |

| Governing Law | The form is governed by Georgia Code Section 48-7-25, which deals with the taxation of unrelated business income. |

| Tax Rate | Unrelated business income is taxed at a rate of 6%, as stipulated by Georgia Code Section 48-7-25(c). |

| Due Date | The return is due on or before the date of the Federal Form 990-T as provided under the Internal Revenue Code. |

| Filing Requirements | Every exempt organization that is required to file a Form 990-T with the Federal Government and has unrelated trade or business income from Georgia sources must file a Georgia Form 600-T. |

Guide to Using Georgia 600 T

Filling out the Georgia Form 600-T is an essential process for exempt organizations in Georgia that are reporting unrelated business income. This form is necessary to comply with state tax regulations and must be completed accurately to ensure compliance. The process may seem daunting at first, but by following the steps outlined below, organizations can complete the form confidently and efficiently.

- Start by gathering all necessary documents, including the Federal Form 990-T and any related schedules and extensions.

- Enter the taxable year's beginning and ending dates at the top of the form.

- Provide the name of the organization and, if applicable, the name of the fiduciary.

- Include the Federal Employer Identification Number (EIN) or the trust’s identification number if the organization is an employees’ trust described in section 401(a) and exempt under section 501(a).

- Fill out the address fields, including the mailing address to which correspondence should be sent, and the physical address of the organization if different from the mailing address.

- Indicate the NAICS Code that applies to the organization’s primary unrelated business activity.

- Enter the date of the current IRS code section exemption letter.

- Proceed to Schedule 1:

- Enter the unrelated business taxable income reported on Federal Form 990-T and attach a copy of it.

- Add any additions and subtractions as required to calculate the Georgia unrelated business taxable income.

- In Schedule 2, compute the Georgia unrelated business income tax:

- Multiply the amount from Schedule 1, line 5, by 6%.

- Subtract any credits, payments, and withholding credits applicable.

- Include interest due, any penalties for underpayment, and other penalties, then calculate the balance of tax, interest, and penalties due with the return.

- Indicate whether any overpayment is to be credited to the next year’s estimated tax or refunded.

- Complete the declaration section, ensuring that an officer of the organization signs and dates the form. If someone other than a taxpayer prepares the return, their information and signature should also be included.

- Don't forget to attach a copy of the Federal Form 990-T along with supporting schedules and any extensions.

After completing the form, review it thoroughly to ensure all information is accurate and complete. Then, mail it to the indicated address by the deadline specified in the instructions. If an extension is needed, submit Form IT-303 before the due date. This careful attention to detail ensures compliance with Georgia’s tax regulations for exempt organizations.

Obtain Clarifications on Georgia 600 T

- What is the purpose of the Georgia Form 600-T?

The Georgia Form 600-T serves as the Unrelated Business Income Tax Return for exempt organizations operating within the state. Its primary purpose is to tax income that is unrelated to the exempt purposes of such organizations, in compliance with Georgia Code Section 48-7-25. This form is necessary when these entities generate revenue from business activities that do not directly relate to their tax-exempt purposes.

- Who is required to file the Georgia Form 600-T?

Any exempt organization required to file a Form 990-T with the Federal Government, due to receiving unrelated trade or business income from Georgia sources, must file the Georgia Form 600-T. This includes charities, non-profits, and other organizations enjoying tax-exempt status but engaging in income-generating activities outside their primary exempt functions.

- When is the Georgia Form 600-T due?

The deadline for submitting the Georgia Form 600-T coincides with the due date of the organization's Federal Form 990-T. The specific date hinges on the organization's tax year but typically follows the federal schedule for such returns.

- Where should the Georgia Form 600-T be filed?

The completed form should be mailed to the Georgia Department of Revenue, Processing Center, P.O. Box 740397, Atlanta, GA 30374-0397. This ensures it reaches the correct office for processing within the state's revenue department.

- Can an organization request an extension for filing the Georgia Form 600-T?

Yes, organizations may request a reasonable extension for filing by submitting Form IT-303 before the original deadline. Moreover, if the organization has already secured a federal filing extension, attaching a copy of the federal extension request suffices for a state extension. However, the law caps the extension at no more than six months past the original deadline.

- What is the tax rate applied to unrelated business income?

The unrelated business income reported on the Georgia Form 600-T is taxed at a rate of 6%, as mandated by Georgia Code Section 48-7-25(c).

- How should income and expenses be allocated for multi-state organizations?

Organizations operating in multiple states should allocate and apportion income and expenses to accurately reflect the portion attributable to Georgia. This process ensures the state taxes only the income derived from or connected to Georgia sources. Adequate documentation and support for these allocations should accompany the filed Form 600-T.

- What penalties and interest may apply?

Various penalties apply for delinquencies in filing or payment, including a delinquent filing penalty of 5% per month of the unpaid tax, a delinquent payment penalty of 0.5% per month, and, for underpayments due to negligence or fraud, penalties of 5% and 50%, respectively. Interest on unpaid taxes accrues at a rate of 12% per year from the due date until payment. The combined total of delinquency penalties cannot exceed 25% of the unpaid tax.

Common mistakes

Filling out the Georgia 600-T form can seem straightforward, but a few common slip-ups can cause headaches down the road. Here's what to watch for:

Not attaching a copy of the Federal 990-T: One of the most common mistakes is forgetting to attach a copy of the Federal Form 990-T along with supporting schedules and any extensions. This is a must-do.

Incorrect accounting method: The form needs to reflect the accounting method you regularly use in your organization's books and records. Switching methods just for this form can lead to discrepancies.

Failing to include the correct Date of current IRS code section exemption letter. This date is crucial for validating your tax-exempt status and the related income.

Not applying for a state extension if you haven't got an IRS extension: If you've been granted an extension by the IRS, you're fine, but if not, you need to apply for one separately with the state of Georgia.

Missing out on deductions and credits: Properly accounting for deductions and credits can significantly reduce your tax liability. It's easy to overlook these.

Miscalculating taxable income: Starting with your federal taxable income, make sure any additions or subtractions specific to Georgia law are correctly calculated to avoid errors in determining your state taxable income.

Not accounting for Withholding Credits (G-2A, G-2LP, and/or G-2RP) properly. These credits can reduce your balance due, so it’s important to claim them if eligible.

Inaccurate payment of estimated tax penalty (UET) or not checking the “UET Annualization Exception attached” box if applicable: This is a specific area that can trip you up if you're not careful about your payments and exemptions.

Avoiding these mistakes not only ensures compliance but can also save your organization from unnecessary penalties and interest. Taking time to double-check your return, attaching all required documentation, and making sure every line is accurate can make a big difference.

Documents used along the form

In the realm of tax obligations for exempt organizations operating in Georgia, understanding the landscape of required filings beyond the Georgia Form 600-T can significantly streamline compliance efforts. This form, specifically tailored for exempt organizations to report their unrelated business income tax in Georgia, functions within a broader ecosystem of documentation essential for thorough and compliant tax filing. A suite of other forms and documents often accompanies the Georgia Form 600-T to ensure comprehensive adherence to Georgia's tax code and to facilitate accurate reporting of an organization's financial activities.

- Federal Form 990-T: This is the federal counterpart to the Georgia Form 600-T and is used by tax-exempt organizations to report unrelated business income at the federal level. It is essential because the Georgia form requires attaching a copy of the Federal 990-T, thereby linking state and federal tax obligations.

- Form IT-303: Used to request an extension of time to file the Georgia Form 600-T. This form is critical for organizations that need additional time to gather necessary information or for those waiting on the completion of their Federal Form 990-T.

- Form G-2A, G-2LP, and G-2RP: These forms relate to withholding credits for nonresident members of the organization. They allow exempt entities to claim credits against the Georgia unrelated business income tax for amounts withheld on behalf of their members.

- Form 600 UET: Required if there's an underpayment of estimated tax by the organization. It helps calculate penalties that may be due for underestimating quarterly tax payments and is integral to ensuring compliance with estimated payment regulations.

- Request for Extension (Federal): Not a form per se, but important documentation nonetheless. If an organization has obtained a federal extension to file Form 990-T, a copy of this request must be attached to the Georgia Form 600-T, circumventing the need for a separate state extension request.

- Allocation and Apportionment Schedules: While not a standardized form, these schedules are often necessary for organizations operating in multiple states. They detail how income and expenses are divided between Georgia and other jurisdictions, supporting the allocation and apportionment claims made on the Form 600-T.

Each of these documents plays a distinct role in the tax filing process, ensuring that exempt organizations meet both state and federal obligations with accuracy and transparency. Understanding their purposes and how they interconnect with the Georgia Form 600-T empowers organizations to navigate the tax landscape more efficiently, minimizing compliance risks while upholding their financial responsibilities.

Similar forms

The IRS Form 990-T is quite similar to the Georgia Form 600-T as it serves the purpose for exempt organizations to report unrelated business income at the federal level. Both forms require detailed income calculations and the reporting of taxable income from activities not related directly to the organization's exempt purpose. Additionally, organizations must attach a copy of their IRS Form 990-T when filing the Georgia Form 600-T, underscoring the direct relationship between these two documents.

Another related document is the Form IT-303, which is the Application for Extension of Time for Filing State Income Tax Returns in Georgia. Much like the mention of extension considerations in the Georgia 600-T instructions, Form IT-303 is used to request more time to file one's state tax returns, including the 600-T, should an organization need it due to reasonable cause. This highlights the administrative processes related to filing deadlines and the parallel requirement for both extensions and end-year filings.

The Form 600 UET (Underpayment of Estimated Tax) is also related to the Georgia Form 600-T, particularly where the instructions for the 600-T mention the need for attaching Form 600 UET in scenarios of underpayment penalties. Both forms intersect in their goal to reconcile outstanding tax obligations, with the 600 UET specifically addressing the estimated tax component for organizations.

Finally, the Form G-2A, G-2LP, and/or G-2RP are mentioned within the Form 600-T instructions under withholding credits. These forms relate to Georgia Tax Withholding for different contexts (G-2A for affidavits, G-2LP for partnerships, and G-2RP for residents) and are necessary for calculating the accurate withholding credits to be reported on the 600-T. This connection highlights the integration of withholding practices with the reporting of unrelated business income tax.

Dos and Don'ts

When it comes to dealing with the Georgia 600-T form, which is the Exempt Organization Unrelated Business Income Tax Return, there are certain practices that can make the process smoother and others that should be avoided. Below are seven key dos and don'ts that can help ensure accuracy and compliance when handling this form:

- Do ensure a copy of the Federal Form 990-T and all supporting schedules, including any extensions, are attached to your return. This is a crucial step for compliance.

- Do verify that all the information from the Federal Form 990-T, such as unrelated business taxable income, is accurately reported on the Georgia Form 600-T.

- Do apply for an extension if necessary by filing Form IT-303 before the due date. Remember, providing a copy of your Federal extension can simplify this process.

- Do carefully calculate your tax obligation using Georgia’s specific rate for unrelated business income, which is set at 6%.

- Do not overlook the importance of accurately calculating additions and subtractions on your return to determine the correct Georgia unrelated business taxable income.

- Do not forget to include pertinent details such as the name of the organization, address, and Federal Employer ID No., ensuring the form is filled out in its entirety.

- Do not delay the filing and payment processes. Penalties for delinquent filing and payment can accrue quickly, so it's important to meet all deadlines to avoid unnecessary fees.

By adhering to these guidelines, organizations can navigate the complexities of the Georgia 600-T form more effectively, avoiding common pitfalls and ensuring that they remain compliant with state requirements for reporting unrelated business income.

Misconceptions

When discussing the Georgia Form 600-T, there are several misconceptions that may lead to confusion among exempt organizations required to report unrelated business income. Clarifying these misconceptions is crucial to ensure accurate and compliant tax reporting.

- Applicability only to certain organizations: Some believe that only specific types of organizations need to file Form 600-T, when in fact, any exempt organization with unrelated business income from Georgia sources must file.

- No need for federal compliance: There's a misconception that if an organization files Form 600-T, it need not comply with federal filing requirements. However, organizations must file a Form 990-T with the Federal Government in addition to the state form.

- Fixed tax rate misunderstanding: It's wrongly assumed that all unrelated business income is taxed at a variable rate, but under Georgia Code Section 48-7-25(c), the income is taxed at a fixed rate of 6%.

- Extension deadlines are flexible: Some think that extension deadlines are merely suggestive and can be extended further upon request. The truth is Georgia Law prohibits extension of over six months from the due date of the return.

- Penalties are negotiable: A common misconception is that penalties for late filing or payment can be negotiated or waived upon explanation. Penalties and interest are mandated by law, with specific calculations for delinquencies.

- All income is reportable: There's a misunderstanding that all forms of income must be reported on Form 600-T. Only unrelated business income, as defined by IRS and Georgia regulations, needs to be reported.

- Amendments due to IRS changes exempt from penalties: Some organizations believe amending a return due to IRS audit findings exempts them from penalties. While amendments may adjust tax liabilities, penalties for original inaccuracies may still apply.

- No necessity for Federal 990-T attachment: Another misconception is that attaching a copy of the Federal Form 990-T and its schedules is optional. Georgia regulations require these federal documents to accompany the 600-T form.

- Interest rates are standard: The belief that interest on underpaid tax is calculated at a standard rate for all situations is incorrect. Georgia sets a specific annual rate for underpaid tax interest calculations.

- Electronic filing accommodations: Some assume that electronic filing options are available for all aspects of the 600-T process. Currently, specific submission guidelines, including paper mailing addresses, are provided and must be followed unless otherwise stated by the Georgia Department of Revenue.

Addressing these misconceptions is vital for organizations to maintain compliance and avoid unnecessary penalties. It's always advisable for organizations to consult with a tax professional or the Georgia Department of Revenue directly for accurate information and guidance on filing the Georgia Form 600-T.

Key takeaways

When it comes to the Georgia 600-T form, there are several key points that organizations need to understand. This form is crucial for exempt organizations operating in Georgia because it addresses the taxation of unrelated business income. Below are eight key takeaways that every organization should consider:

- Filing Requirements: Any exempt organization required to file a Form 990-T with the Federal Government, due to generating unrelated business income from sources within Georgia, must also file the Georgia Form 600-T.

- Due Date and Mailing Address: The submission of the Form 600-T should coincide with the Federal Form 990-T's due date. It must be mailed to the Georgia Department of Revenue Processing Center at P.O. Box 740397, Atlanta, GA 30374-0397.

- Extension of Time: Organizations can apply for an extension using Form IT-303 before the due date. If an extension has already been granted by the IRS for the federal return, attaching a copy of the federal extension request to the Georgia return suffices.

- Tax Rate: Unrelated business income is taxed at 6%, as stipulated by Georgia Code Section 48-7-25(c).

- Accounting Method: The organization must use its regular accounting method for reporting, which should clearly reflect taxable income.

- Allocation and Apportionment: For organizations generating unrelated business income both within Georgia and elsewhere, it is necessary to properly allocate and apportion income and expenses to accurately report Georgia unrelated business taxable income.

- Penalties and Interest: Penalties may be applied for delinquent filing, delinquent payment, negligent underpayment, and fraudulent underpayment. Interest accrues at 12% per year from the due date of payment until paid. Certain penalties, like those for delinquent filing and payment, cannot collectively exceed 25% of the unpaid tax by the original due date.

- Attachment Required: A copy of the Federal Form 990-T, along with supporting schedules (and any extensions), must be attached to the Georgia Form 600-T upon submission.

Understanding these key takeaways helps ensure that exempt organizations comply with Georgia's taxation regulations for unrelated business income. Proper preparation and attention to these details can mitigate the risk of penalties and ensure the smooth processing of the Form 600-T.

Popular PDF Forms

Handicap Form - The form also facilitates requests from businesses or institutions that primarily transport disabled individuals, adhering to specific criteria set by Georgia law.

What Is a Rule Nisi in Georgia - Demarcates the serious transition from informal negotiations to a formal court ruling on the matter at hand.

Georgia Car Title Template - Applying for a salvage title in Georgia? The MV-1S form guides you through the process, including information on fees and how to submit.