Free Georgia Att 21 Template in PDF

Understanding the intricacies of compliance within the tobacco industry in Georgia necessitates a thorough grasp of various regulatory documents, one of which is the Georgia ATT-21 form. As a bond crucial for licensed wholesale tobacco distributors, this document plays a pivotal role in ensuring that distributors are financially responsible for the tobacco tax stamps they purchase. The ATT-21 form, revised in December 2009, binds the distributor and an appointed surety to the Georgia Revenue Commissioner and the Department of Revenue for a predetermined amount, essentially guaranteeing full payment for all tobacco tax stamps acquired within a fiscal year ending June 30. This bond, which must be signed by the surety's attorney in fact, with a corporate seal affixed, signifies a commitment to comply with the state’s regulations, specifically an Act approved on March 4, 1970. Furthermore, it outlines provisions for bond cancellation, maintaining the surety’s liability for any covered purchases or acts prior to the cancellation's effective date, which is sixty days post notice receipt by the Revenue Commissioner and the principal distributor. The bond not only underscores the legal and financial obligations of tobacco distributors but also demonstrates the state's efforts to regulate and ensure compliance within the industry, with the ultimate goal of protecting the public interest and maintaining a fair market environment.

Form Sample

|

|

Rev. (12/09) |

BOND NO. |

|

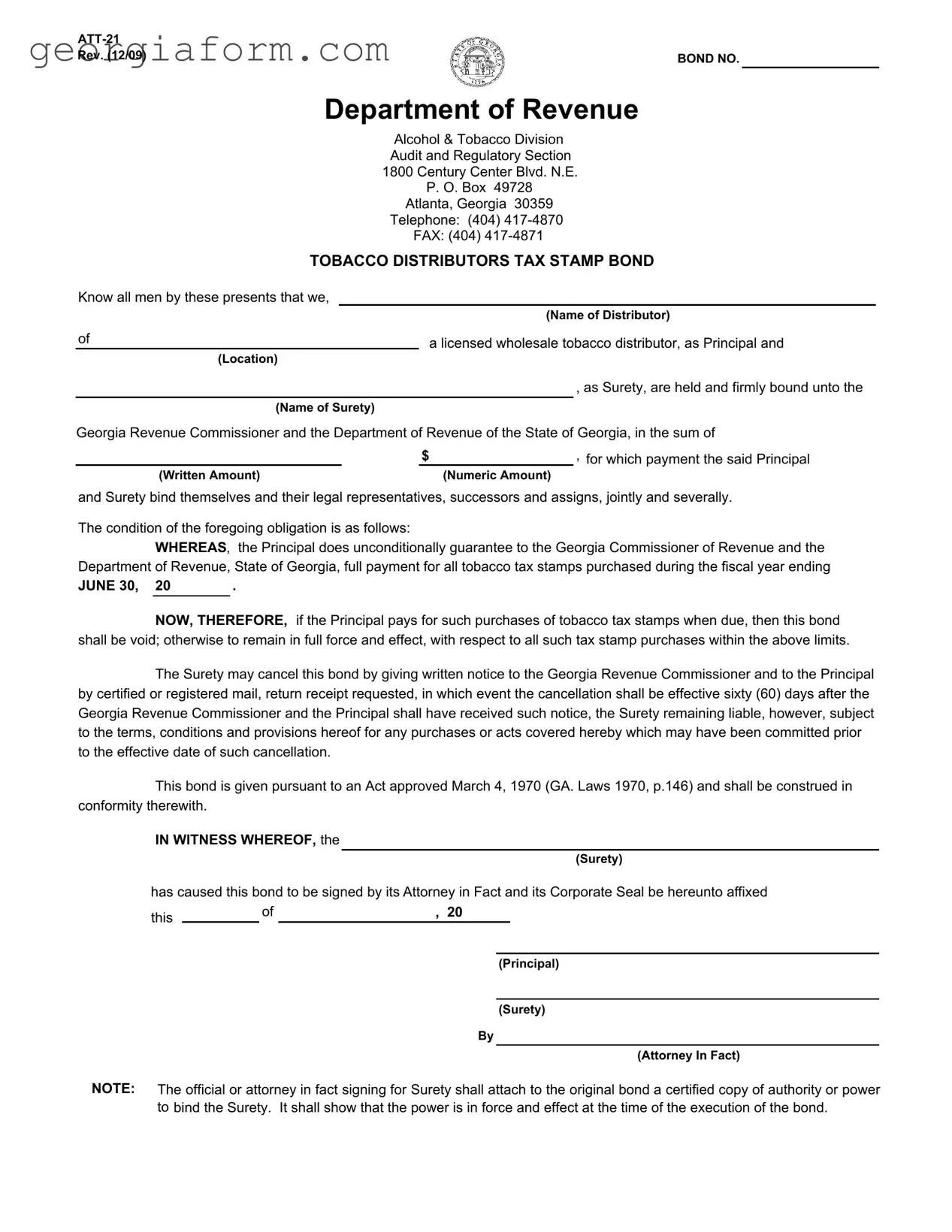

Department of Revenue

Alcohol & Tobacco Division

Audit and Regulatory Section

1800 Century Center Blvd. N.E.

P. O. Box 49728

Atlanta, Georgia 30359

Telephone: (404)

FAX: (404)

TOBACCO DISTRIBUTORS TAX STAMP BOND

Know all men by these presents that we,

(Name of Distributor)

of |

|

a licensed wholesale tobacco distributor, as Principal and |

|||

(Location) |

|

|

|||

|

|

|

|

|

, as Surety, are held and firmly bound unto the |

(Name of Surety) |

|

|

|||

Georgia Revenue Commissioner and the Department of Revenue of the State of Georgia, in the sum of |

|||||

|

|

$ |

|

, for which payment the said Principal |

|

(Written Amount) |

(Numeric Amount) |

||||

and Surety bind themselves and their legal representatives, successors and assigns, jointly and severally.

The condition of the foregoing obligation is as follows:

WHEREAS, the Principal does unconditionally guarantee to the Georgia Commissioner of Revenue and the Department of Revenue, State of Georgia, full payment for all tobacco tax stamps purchased during the fiscal year ending

JUNE 30, 20 |

. |

|

|

|

|

NOW, THEREFORE, if the Principal pays for such purchases of tobacco tax stamps when due, then this bond shall be void; otherwise to remain in full force and effect, with respect to all such tax stamp purchases within the above limits.

The Surety may cancel this bond by giving written notice to the Georgia Revenue Commissioner and to the Principal by certified or registered mail, return receipt requested, in which event the cancellation shall be effective sixty (60) days after the Georgia Revenue Commissioner and the Principal shall have received such notice, the Surety remaining liable, however, subject to the terms, conditions and provisions hereof for any purchases or acts covered hereby which may have been committed prior to the effective date of such cancellation.

This bond is given pursuant to an Act approved March 4, 1970 (GA. Laws 1970, p.146) and shall be construed in conformity therewith.

IN WITNESS WHEREOF, the

(Surety)

has caused this bond to be signed by its Attorney in Fact and its Corporate Seal be hereunto affixed

this |

|

of |

, 20 |

|

|

|

(Principal)

(Surety)

By

(Attorney In Fact)

NOTE: The official or attorney in fact signing for Surety shall attach to the original bond a certified copy of authority or power to bind the Surety. It shall show that the power is in force and effect at the time of the execution of the bond.

File Overview

| Fact Name | Description |

|---|---|

| Form Designation | The form is known as ATT-21, with a revision date of December 2009. |

| Purpose | It serves as a Tobacco Distributors Tax Stamp Bond form. |

| Governing Body | Administered by the Georgia Department of Revenue, Alcohol & Tobacco Division, Audit and Regulatory Section. |

| Financial Obligation | The bond ensures the payment for all tobacco tax stamps purchased during the specified fiscal year. |

| Condition for Voidance | The bond will be void if the principal pays for the purchased tobacco tax stamps when due. |

| Surety Cancellation Rights | The Surety has the right to cancel the bond by giving written notice 60 days in advance, remaining liable for any prior commitments. |

| Governing Law | The bond is issued pursuant to an Act approved on March 4, 1970 (GA. Laws 1970, p.146), which guides its interpretation and enforcement. |

Guide to Using Georgia Att 21

Filling out the Georgia Att 21 form is a crucial step for tobacco distributors to ensure compliance with state requirements for tax stamp purchases. This document acts as a bond, promising that the distributor will fully pay for all tobacco tax stamps bought within a fiscal year. It's a straightforward process, but attention to detail is imperative to avoid any errors that could lead to delays or issues with the Georgia Department of Revenue. Here's how to correctly complete the form to ensure a smooth submission process.

- Start by writing the name of the distributor in the space provided after "Know all men by these presents that we,". This is the licensed wholesale tobacco distributor acting as the Principal in this bond.

- Enter the location of the distributor next to their name.

- Fill in the name of the Surety. This is the entity or individual who guarantees the bond, positioned right after "as Surety" in the text.

- Specify the bond amount in both words ("Written Amount") and numerically ("Numeric Amount") where indicated. This represents the total sum for which the Surety and Principal are bound to the Commissioner of Revenue and the Department of Revenue of the State of Georgia.

- Indicate the fiscal year ending date as June 30, followed by the year, in the space after "ending JUNE 30," to establish the period covered by this bond.

- At the bottom of the form, ensure that the Surety's name is included again where it reads "(Surety) has caused this bond to be signed.."

- Insert the date the bond is signed in the space provided. This must include the day, month, and year of execution.

- The Principal and Surety should sign their names where indicated. If the Surety is an organization, the authorized official or attorney-in-fact must sign on its behalf.

- Remember, the official or attorney-in-fact signing for the Surety must attach a certified copy of the authority or power to bind the Surety. Ensure this document is current and accurately reflects the signee's capacity to execute the bond.

After completing these steps, review the form for accuracy and completeness. Missing or incorrect information could result in processing delays or the bond being deemed invalid. Submit the completed form along with any required attachments to the address indicated at the top of the form, ensuring it reaches the Department of Revenue's Alcohol & Tobacco Division. Prompt submission can help avoid any compliance issues, securing your status as a licensed distributor within Georgia's regulatory framework.

Obtain Clarifications on Georgia Att 21

What is the Georgia ATT-21 Form?

The Georgia ATT-21 Form, known as the Tobacco Distributors Tax Stamp Bond, is a legal document required by the Georgia Department of Revenue, Alcohol & Tobacco Division. It serves as a bond between a licensed wholesale tobacco distributor (the principal) and the Department of Revenue for the State of Georgia. This bond guarantees the full payment for all tobacco tax stamps purchased by the distributor during the fiscal year.

Who needs to file the ATT-21 Form in Georgia?

Any business acting as a wholesale distributor of tobacco products in Georgia must file the ATT-21 Form. This includes entities that purchase tobacco tax stamps, which are necessary for the legal sale of tobacco products within the state.

What is the purpose of the bond?

The bond ensures that the distributor will fulfill their financial obligations related to the purchase of tobacco tax stamps from the Georgia Department of Revenue. Should the distributor fail to pay for the stamps when due, the bond remains in effect, securing the owed amount to the commissioner of revenue.

How much does the bond cost?

The bond amount varies and is specified by the Georgia Department of Revenue based on the distributor's purchase volume or other determining factors. It is the total monetary guarantee that the principal and surety offer to the Georgia Revenue Commissioner and the Department of Revenue for the payment of the tobacco tax stamps.

Can the Surety cancel the bond? If so, how?

Yes, the surety has the right to cancel the bond. Cancellation requires written notice sent to both the Georgia Revenue Commissioner and the principal distributor by certified or registered mail, return receipt requested. The cancellation becomes effective sixty days after the receipt of the notice. However, the surety remains liable for any purchases or actions taken prior to the cancellation date.

What legislation governs the ATT-21 Form?

The ATT-21 Form and the obligations it outlines are governed by an Act approved on March 4, 1970 (GA. Laws 1970, p.146). The form and the associated bond are construed in conformity with this legislation, ensuring compliance with state laws regarding the sale and distribution of tobacco products.

What are the requirements for the surety's signature?

The surety must ensure that the bond is signed by its attorney in fact, and it must have its corporate seal affixed. Additionally, a certified copy of the authority or power allowing the attorney in fact to bind the surety must be attached to the original bond. This certification proves that the surety's representative has the right to enter into the bond agreement on behalf of the surety at the time of execution.

Common mistakes

When filling out the Georgia ATT-21 form, certain common missteps can lead to complications in the processing and acceptance of the form. Awareness and avoidance of these errors are crucial for ensuring the form is correctly completed:

- Incorrect or Incomplete Principal and Surety Information: Applicants often fail to provide complete information for the distributor (Principal) and the surety. This includes the name of the distributor, location, and the name and address of the surety. It is imperative to thoroughly check that all sections are accurately filled out to avoid delays.

- Discrepancies in the Bond Amount: There is a common error in not matching the written amount of the bond with its numeric representation. Consistency between these two is necessary to validate the bond's value, ensuring the Department of Revenue understands the exact bond amount being guaranteed.

- Failure to Attach Required Documents: The form stipulates that the official or attorney in fact signing for the surety must attach a certified copy of authority or power to bind the Surety. Sometimes, this crucial document is overlooked or forgotten, questioning the authorization to commit the surety and potentially invalidating the bond application.

- Lack of Signatures and Seal: A frequent mistake includes omitting the necessary signatures and corporate seal on the bond. The surety must have the bond signed by its Attorney in Fact, and the corporate seal must be affixed to the document. These formalities are critical for the legal binding of the bond.

Understanding and addressing these potential pitfalls upfront can significantly streamline the process of successfully completing and submitting the Georgia ATT-21 form. Each step, from ensuring all information is complete and accurate, to attaching necessary documentation, to executing the bond properly, is vital for compliance with the state's requirements.

Documents used along the form

When dealing with tobacco distribution in Georgia, particularly regarding tax stamp bonds as outlined by Georgia's ATT-21 form, several accompanying forms and documents are frequently utilized to ensure compliance, legal clarity, and thorough record-keeping. These forms not only support the initial bond but also facilitate various operational, regulatory, and financial processes essential for distributors operating within the state. By understanding these documents, distributors can navigate the legal and administrative landscape more effectively.

- Application for Tobacco Distributor License: Before a distributor can even qualify for the ATT-21 form, they must first apply for and obtain a tobacco distributor's license. This document collects business information, ownership details, and the scope of operations.

- Power of Attorney (POA) Documentation: Anytime a surety is involved, as is the case with the ATT-21 form, there often needs to be a power of attorney document. This legal document authorizes the attorney-in-fact to sign the bond and undertake actions on behalf of the principal, proving their legal authority to do so.

- Financial Statements: Comprehensive financial statements are typically required to assess the financial health of the distributor. These documents provide insight into the distributor’s ability to meet financial obligations, including those related to tobacco tax stamps.

- Compliance Certification: A document that asserts the distributor's compliance with state laws and regulations, confirming their understanding and adherence to the requirements for distributing tobacco products responsibly and legally.

- Surety Bond Agreement: Besides the ATT-21, a more detailed surety bond agreement might be necessary to specify the terms, conditions, and obligations of both the principal and the surety beyond the initial bond form.

- Annual License Renewal Form: To maintain an active distributor license in Georgia, an annual renewal form must be submitted. This ensures that the distributor's information is up-to-date and that they remain in good standing with the state.

- Notice of Bond Cancellation: If a bond like the one described in the ATT-21 form needs to be cancelled, a formal notice of cancellation must be filed. This document will include details about the bond, reasons for cancellation, and the effective date of such cancellation.

Each of these documents plays a pivotal role in supporting the operational, financial, and regulatory needs of tobacco distributors in Georgia. Combining the ATT-21 form with these additional forms ensures a seamless flow of activities, from licensing to bond execution and compliance, fostering a responsible and regulation-abiding business environment.

Similar forms

The Georgia ATT-21 form, serving as a Tobacco Distributors Tax Stamp Bond, shares similarities with various other documents pertaining to financial and legal assurances in the business and regulatory landscape. These documents, though diverse in their application, align in their core function of providing a security mechanism against failure to comply with specific obligations. Below are seven documents similar to the Georgia ATT-21 form:

- Performance Bond: This type of bond is common in the construction industry and large contract-based projects. Similar to the ATT-21, a Performance Bond provides a guarantee to the project owner (obligee) that the contractor (principal) will perform according to the terms of the contract. If the contractor fails to do so, the bond will cover any financial losses or the cost of completion by another contractor.

- License and Permit Bonds: These are required by various state departments and local municipalities for businesses in certain industries to operate legally. Like the ATT-21, which ensures compliance with tobacco tax stamp regulations, License and Permit Bonds ensure adherence to local, state, or federal regulations applicable to a specific license or permit.

- Customs Bond: Required for importers to guarantee compliance with import laws and regulations. The Customs Bond and ATT-21 share the guarantee element, ensuring that the principal adheres to specific regulations and covers any dues or penalties in case of non-compliance.

- Fidelity Bond: It provides protection against losses that occur from fraudulent acts by specified individuals. Although focused on employee dishonesty, the similarity with the ATT-21 lies in its protective function, safeguarding assets against unforeseeable acts that could lead to financial losses.

- Excise Tax Bond: This bond is required for businesses that manufacture, sell, or warehouse goods subject to excise taxes. Similar to the ATT-21, an Excise Tax Bond guarantees the payment of taxes due to the government, ensuring compliance with tax regulations.

- Surety Bond: Serving as a broad category that includes the ATT-21 form, Surety Bonds involve three parties and guarantee the performance of an obligation or compliance with law or contractual terms. The ATT-21 is a specific type of Surety Bond tailored to the tobacco industry's regulatory requirements.

- Bid Bond: Required during the bidding process on many public projects, a Bid Bond ensures that the contractor submitting the bid will enter into the contract and perform the work as specified, or pay a penalty amount. This concept mirrors the ATT-21's function, which ensures the tobacco distributor adheres to the commitment of paying taxes on tobacco products.

These documents, although tailored to different sectors and purposes, share the fundamental purpose of ensuring adherence to certain obligations through a financial guarantee provided by the principal or a surety company. The overarching goal is to mitigate risk, whether it be related to project completion, regulatory compliance, or financial commitments.

Dos and Don'ts

When filling out the Georgia ATT-21 form, individuals and businesses must adhere to a set of guidelines to ensure the process is performed correctly. Observing these do's and don'ts will facilitate a smoother submission to the Department of Revenue Alcohol & Tobacco Division.

Do's:

- Ensure all information is accurate and complete, including the full name of the distributor and the surety.

- Write the bond amount in both words and numbers to prevent confusion or alteration.

- Provide the fiscal year ending date for which the bond will cover tobacco tax stamp purchases.

- Sign the bond form as the Principal by the authorized official or attorney in fact of the surety company.

- Attach a certified copy of the authority or power to bind the Surety, verifying its validity at the time of the bond's execution.

- Send the completed form and attachments to the provided address of the Department of Revenue Alcohol & Tobacco Division.

- Use certified or registered mail for submission to ensure receipt and tracking.

- Keep a copy of the completed form and any correspondence for your records.

Don'ts:

- Do not leave any sections blank. Incomplete forms may result in delays or rejection.

- Avoid using unclear or illegible handwriting if filling out the form manually.

- Do not forget to include the seal of the surety company if applicable.

- Do not submit the form without verifying all information for accuracy and completeness.

- Avoid missing the deadline for bond submission relevant to the fiscal year.

- Do not fail to update the Georgia Revenue Commissioner and the Principal in case of bond cancellation or changes.

- Do not overlook the requirement to notify both the Georgia Revenue Commissioner and the Principal via certified or registered mail if the Surety intends to cancel the bond.

- Do not misunderstand the bond's terms, conditions, and provisions. Ensure full comprehension before submission.

Misconceptions

There are several misconceptions surrounding the Georgia ATT-21 form, a crucial document for tobacco distributors in the state. Let's clarify some of the most common misunderstandings.

- The ATT-21 is only for tobacco retailers. This is incorrect. The form is specifically designed for wholesale tobacco distributors, not retailers. Its main purpose is to bind the distributor and a surety to the Georgia Revenue Commissioner, ensuring the payment for tobacco tax stamps.

- It’s a simple registration form. The ATT-21 is actually a bond form, not just a registration document. It is a legal agreement that guarantees the distributor's financial obligation to pay for the tobacco tax stamps purchased.

- Any surety can secure the bond. Not exactly. A surety involved in securing the bond must be recognized and authorized to undertake such responsibilities in the State of Georgia. It’s not just any third party but typically a financial institution or surety company that meets specific criteria set by the state.

- The bond amount is fixed. The bond amount varies and is determined based on several factors, including the distributor’s sales volume or other criteria as defined by the Georgia Department of Revenue. It is not a standard fixed rate for all.

- Completing the ATT-21 form finalizes your obligations. Completing the form is a step in the process but not the end. The distributor and the surety have ongoing obligations, including possible adjustments to the bond amount and ensuring timely payments for purchased tax stamps.

- The form is only applicable for a single fiscal year. While the bond mentions coverage for purchases during a fiscal year, its relevance spans beyond just a year until any obligations outlined under the bond are fully met or the bond is officially cancelled according to the terms specified within the document.

- Cancellation of the bond is immediate upon notice. Actually, the bond cancellation becomes effective 60 days after the Georgia Revenue Commissioner and the Principal receive the notice. The surety remains liable for any acts or purchases made prior to the cancellation’s effective date.

- Any modifications to the bond are prohibited. Modifications can be made to the bond, especially concerning the bond amount or terms, provided these changes are communicated properly and reflect the current operations of the distributor. The key is ensuring all changes are officially documented and communicated to the relevant parties.

- The bond absolves distributors of legal responsibilities. While the bond covers financial obligations related to the purchase of tobacco tax stamps, it does not absolve the distributor or the surety of other legal responsibilities and compliance requirements under Georgia law.

- The ATT-21 form is the only document needed for tobacco distribution. This is a myth. Distributors might need to complete additional forms and obtain various licenses or permits, in compliance with both state and federal regulations, before legally distributing tobacco products in Georgia.

Understanding the Georgia ATT-21 form and its requirements helps ensure that tobacco distributors comply with state laws and regulations, avoiding potential legal and financial pitfalls.

Key takeaways

Filling out and using the Georgia ATT-21 form is crucial for tobacco distributors operating within the state. Here are six key takeaways to ensure compliance and avoid legal complications:

- Ensure accurate representation: The ATT-21 form requires the distributor's name and location as the Principal and identifies the Surety. Providing accurate and truthful information is essential for the bond's validity.

- Understand the bond amount: The bond amount, both written and numeric, signifies the financial commitment of the Principal and Surety to the Georgia Revenue Commissioner and the Department of Revenue. This figure should be carefully determined to comply with state regulations.

- Payment of tobacco tax stamps: The principal condition of the bond is the guarantee of full payment for all tobacco tax stamps purchased by the distributor during the specified fiscal year. Failure to meet this condition can invalidate the bond and lead to financial liabilities.

- Cancellation process: The Surety has the right to cancel the bond, subject to a 60-day notice period to both the Georgia Revenue Commissioner and the Principal. Understanding the cancellation process and deadlines is important for both the Surety and Principal to manage their obligations effectively.

- Legislative compliance: The bond is issued under specific Georgia legislation (Act approved March 4, 1970). Distributors and their sureties should be familiar with this legal framework to ensure full compliance and avoid any legal misunderstandings or penalties.

- Execution and documentation: When signing the bond, the Surety must attach a certified copy of the authority or power to bind the Surety. This verifies that the individual signing has the legal authority to do so, adding a layer of legal security for all parties involved.

By adhering to these key points, tobacco distributors and their sureties can navigate the obligations and requirements of the Georgia ATT-21 form more effectively, ensuring lawful operation within the state.

Popular PDF Forms

Ga Workers Compensation - Necessary for formally designating claims as catastrophic, appealing rehabilitation decisions, or addressing penalties and attorney fees.

Panel of Physicians Georgia Form - By clearly identifying the represented party and legal counsel, it contributes to a more organized and efficient dispute resolution process.

Renewal Food Stamps - Asks for detailed information regarding any convictions related to SNAP benefits misuse.