Free Georgia Hotel Tax Template in PDF

In the state of Georgia, a significant provision caters to the state or local government officials and employees who are traveling on official business. This provision centers around an important document known as the Certificate of Exemption of Local Hotel/Motel Excise Tax, introduced through Act Number 621 amending the Official Code of Georgia Annotated Section 48-13-51 since April 2, 1987. This legislative change ensures that these government representatives are exempt from paying county or municipal excise taxes on lodging, often simplistically referred to as the local hotel/motel tax. For operators of hotels and motels within Georgia, this means that upon proper verification of the government official’s or employee’s status, and with the presentation of the specified form, they are required to grant a tax exemption to the individual. The form details acceptable payment methods for the exemption and mandates the maintenance of a copy of the exemption form with the hotel tax records, to document the individual’s exempt status. This process not only necessitates close attention to compliance from hotel and motel operators but also offers a clear protocol for government officials and employees to benefit from tax exemptions, ensuring that the financial aspects of their official travel are handled efficiently. Additionally, it's pertinent to note the exemption also applies to Georgia State Sales Tax under specific conditions, further easing the travel expense burden for those serving the state or local government on official duty.

Form Sample

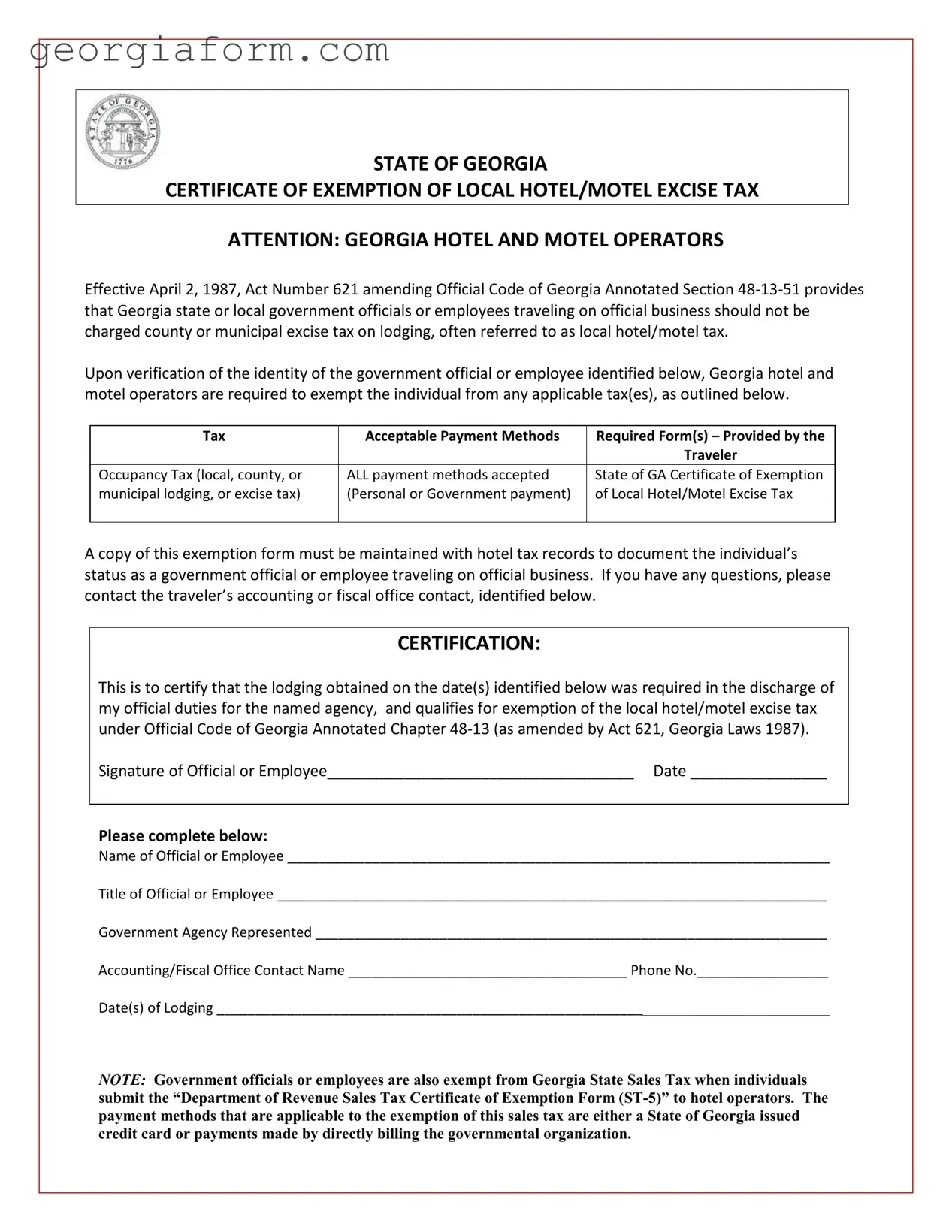

STATE OF GEORGIA

CERTIFICATE OF EXEMPTION OF LOCAL HOTEL/MOTEL EXCISE TAX

ATTENTION: GEORGIA HOTEL AND MOTEL OPERATORS

Effective April 2, 1987, Act Number 621 amending Official Code of Georgia Annotated Section

Upon verification of the identity of the government official or employee identified below, Georgia hotel and motel operators are required to exempt the individual from any applicable tax(es), as outlined below.

Tax |

Acceptable Payment Methods |

Required Form(s) – Provided by the |

|

|

Traveler |

|

|

|

Occupancy Tax (local, county, or |

ALL payment methods accepted |

State of GA Certificate of Exemption |

municipal lodging, or excise tax) |

(Personal or Government payment) |

of Local Hotel/Motel Excise Tax |

|

|

|

A copy of this exemption form must be maintained with hotel tax records to document the individual’s status as a government official or employee traveling on official business. If you have any questions, please contact the traveler’s accounting or fiscal office contact, identified below.

CERTIFICATION:

This is to certify that the lodging obtained on the date(s) identified below was required in the discharge of my official duties for the named agency, and qualifies for exemption of the local hotel/motel excise tax under Official Code of Georgia Annotated Chapter

Signature of Official or Employee____________________________________ Date ________________

Please complete below:

Name of Official or Employee ______________________________________________________________________

Title of Official or Employee _______________________________________________________________________

Government Agency Represented __________________________________________________________________

Accounting/Fiscal Office Contact Name ____________________________________ Phone No._________________

Date(s) of Lodging _______________________________________________________________________________

NOTE: Government officials or employees are also exempt from Georgia State Sales Tax when individuals submit the “Department of Revenue Sales Tax Certificate of Exemption Form

File Overview

| Fact | Description |

|---|---|

| Legislation Date | Effective from April 2, 1987, the exemption has been provided under Act Number 621. |

| Governing Law | Official Code of Georgia Annotated Section 48-13-51, as amended by Act 621, Georgia Laws 1987. |

| Eligible Individuals | Georgia state or local government officials or employees traveling on official business are eligible for tax exemption. |

| Tax Exemption Scope | Exemption applies to county or municipal excise tax on lodging, often referred to as local hotel/motel tax. |

| Verification Requirement | Hotel and motel operators must verify the identity of the government official or employee for tax exemption. |

| Documentation | State of GA Certificate of Exemption of Local Hotel/Motel Excise Tax must be provided and maintained for records. |

| Additional Sales Tax Exemption | Government officials or employees are exempt from Georgia State Sales Tax with a “Department of Revenue Sales Tax Certificate of Exemption Form (ST-5)”. |

Guide to Using Georgia Hotel Tax

Filing out the Georgia Hotel Tax Exemption form is key for Georgia state or local government officials or employees who are traveling on official business to benefit from an exemption on local hotel or motel excise taxes. Effectively utilized, this form ensures that qualifying lodging for official duties is not subject to local occupancy taxes. Here's a simple guide to help navigate through the completion process of the form.

- Verify the traveler’s status: Ensure the individual seeking exemption is a Georgia state or local government official or employee traveling on official business.

- Gather necessary documents: Before filling out the form, make sure you have official identification and any other required document to verify the status of the government official or employee.

- Fill in the certification section: The government official or employee must sign the form and include the date to certify that the lodging was necessary for official duties.

- Complete the personal details: Enter the name, title, and the government agency represented by the official or employee.

- Accounting/Fiscal Office Contact Information: Provide the name and phone number of the relevant contact person in the agency’s accounting or fiscal office.

- Document Lodging Dates: Clearly indicate the date(s) on which lodging was obtained for official duties.

- Understand sales tax exemption: Note that this form exempts qualifying officials from local hotel/motel excise taxes. For exemption from Georgia State Sales Tax, a separate “Department of Revenue Sales Tax Certificate of Exemption Form (ST-5)” must be submitted.

- Choose the appropriate payment method: Remember that all payment methods are accepted for lodging under this exemption, but specific payment methods may apply for sales tax exemption as per the guidance provided.

- Maintain a copy of the completed form: Keep a copy of this exemption form with hotel tax records as documentation of the individual’s eligibility for tax exemption.

By following these steps, eligible Georgia state or local government officials or employees can ensure they are not charged the local hotel/motel excise tax while traveling on official business. Always keep a copy of this exemption form for records and future reference. Should there be any questions regarding the exemption, it's advised to contact the accounting or fiscal office mentioned in the form.

Obtain Clarifications on Georgia Hotel Tax

What is the purpose of the Georgia Hotel Tax form?

The purpose of the Georgia Hotel Tax form, officially known as the Certificate of Exemption of Local Hotel/Motel Excise Tax, is to exempt Georgia state or local government officials or employees from county or municipal excise taxes on lodging while they are traveling on official business. This exemption comes as a result of Act Number 621 which amended Official Code of Georgia Annotated Section 48-13-51, effective since April 2, 1987.

Who is eligible for the tax exemption provided by this form?

The tax exemption is specifically designed for Georgia state or local government officials or employees who are traveling for official government business. This includes trips that are necessary for the discharge of their official duties.

What types of taxes are exempted under this form?

This form exempts eligible individuals from local, county, or municipal lodging taxes, often referred to as hotel or motel excise taxes. It is important to note that this exemption only applies to these specific types of local taxes and does not exempt an individual from other forms of taxation that may apply.

What are the acceptable payment methods to qualify for the tax exemption?

There are no restrictions on the payment methods that can be used to qualify for the lodging tax exemption. This means that both personal payments and payments made directly by the government agency, such as through a government-issued credit card or direct billing arrangements, are acceptable.

What form(s) are required to obtain this tax exemption?

To avail of the tax exemption, the eligible government official or employee must provide the hotel or motel operator with the State of Georgia Certificate of Exemption of Local Hotel/Motel Excise Tax. Additionally, for exemption from Georgia State Sales Tax, the “Department of Revenue Sales Tax Certificate of Exemption Form (ST-5)” must be submitted.

Is documentation required to verify eligibility for the exemption?

Yes, verification of the identity and official status of the government official or employee is required. This can be accomplished through the submission of the exemption form, which includes a certification section that must be filled out, indicating that the lodging is required for official duties.

How should the tax exemption forms be maintained?

Hotel and motel operators are required to retain a copy of the exemption form with their hotel tax records. This documentation serves to verify that the individual was eligible for the tax exemption at the time of their stay.

Who can I contact if I have questions about the exemption?

If there are any questions regarding the exemption, individuals are encouraged to contact the accounting or fiscal office of the government agency represented, as identified in the exemption form. This office can provide additional clarification on eligibility and the proper use of the form.

Are government officials or employees also exempt from Georgia State Sales Tax?

Yes, in addition to the local hotel/motel excise tax exemption, government officials or employees can also be exempt from Georgia State Sales Tax on lodging. However, to obtain this exemption, the proper “Department of Revenue Sales Tax Certificate of Exemption Form (ST-5)” must be presented, and payments must be made either with a State of Georgia issued credit card or by directly billing the governmental organization.

Where can I find these tax exemption forms?

The required forms for tax exemption can be obtained from the relevant government agency's fiscal or accounting office, or by visiting specific Georgia state websites, such as the University of Georgia's business and finance website as indicated in the document provided.

Common mistakes

When filling out the Georgia Hotel Tax form, it's crucial to avoid common mistakes to ensure the process is smooth and the exemption is granted without issues. Four common mistakes that individuals often make on this form include:

Not verifying the identity: The form requires that the identity of the government official or employee be verified before the exemption is applied. Failing to provide proper identification or not ensuring the hotel operator checks this can lead to the exemption being denied.

Incorrect or incomplete payment method details: All payment methods are accepted for the occupancy tax exemption, but the form must clearly indicate whether the payment is personal or made by the government. If this section is filled out incorrectly or left blank, it could result in a refusal of the tax exemption.

Failure to provide required forms: Along with the Georgia Hotel Tax exemption form, government officials or employees must also submit the "Department of Revenue Sales Tax Certificate of Exemption Form (ST-5)" if they wish to be exempt from the Georgia State Sales Tax. Overlooking this requirement will lead to the exemption being incomplete.

Not maintaining a copy of the exemption form: A copy of the exemption form must be maintained with hotel tax records to document the individual's status as a government official or employee traveling on official business. Not keeping this record can lead to complications or disputes about the tax exemption at a later date.

By paying attention to these details and ensuring all the necessary information and documentation are correctly provided and recorded, government officials and employees can avoid these common pitfalls and successfully claim their exemption from the local hotel/motel excise tax in Georgia.

Documents used along the form

When dealing with the nuances of lodgings and accommodations taxation, particularly in the context of Georgia's local hotel/motel excise tax exemptions for state or local government officials on official business, it’s paramount to have a clear understanding of the requisite documentation. The Georgia Hotel Tax form is just the starting point. Various other forms and documents seamlessly accompany it, ensuring compliance and facilitating the exemption process. Below is a list of these supplementary documents, each playing a crucial role in the broader spectrum of tax exemption and record-keeping.

- Department of Revenue Sales Tax Certificate of Exemption (ST-5): This document is crucial for government officials or employees seeking exemption from Georgia State Sales Tax. When presented alongside the Georgia Hotel Tax form, it allows the lodging provider to exempt the individual from the state sales tax on their lodging.

- Government ID or Credentials: Verification of the individual’s identity and their status as a government official or employee is a fundamental step. A government-issued ID or official credentials must accompany the exemption forms to substantiate the claim for tax exemption.

- Official Travel Orders or Assignment Letter: This document clarifies the purpose of the lodging, affirming that the stay is indeed for official government business. It serves as further evidence that the individual qualifies for the tax exemptions.

- Proof of Payment or Billing Arrangement: Whether it’s a receipt of a state-issued credit card payment or documentation of direct billing to the government agency, proof of payment method is essential. It ensures that the payment complies with the criteria for tax exemption eligibility.

- Accommodation Invoice or Lodging Receipt: Detailed documentation of the lodging, including the dates of stay and the amount charged, is necessary for records. This accompanies the exemption forms to provide a complete financial portrait of the lodging expenses.

- Accounting or Fiscal Office Verification Letter: A letter from the traveller’s governmental accounting or fiscal office may sometimes be requested to verify the official travel and ensure all tax exemption criteria are met. This letter would typically confirm the individual’s eligibility and the travel's compliance with government policy.

Understanding and compiling the correct documentation is invaluable for a smooth process in tax exemption for lodging in Georgia. These documents, in conjunction with the Georgia Hotel Tax form, form a comprehensive suite ensuring that government officials and employees traveling on official business are accurately exempt from local hotel/motel excises. Familiarity with these forms not only aids in adherence to Georgia's tax laws but also streamlines the administrative process for both lodging providers and government travelers.

Similar forms

State Sales Tax Exemption Form (ST-5): This document is quite similar to the Georgia Hotel Tax Form, as both aim to exempt specific entities from taxes, in this case, state sales tax versus local hotel/motel excise tax. Like the hotel tax exemption, the sales tax exemption requires official documentation that verifies the eligibility of the individual or entity seeking exemption. Furthermore, both forms necessitate that the exempt party is acting in an official capacity, with the sales tax form specifically catering to entities that are exempt from sales taxes when the purchases are made for official purposes.

Vehicle Rental Tax Exemption Certificate: Similar to the local hotel/motel excise tax exemption, this form exempts government officials from taxes incurred when renting vehicles for official business. Verification of the official’s identity and purpose for the rental is required to qualify for this tax exemption. Both forms serve government employees, ensuring that their official expenditures are minimized by eliminating certain taxes.

Government Request for Taxpayer Identification Number and Certification (W-9 Form): This form, while used in a different context, involves the verification of an entity’s or individual’s status for tax-related purposes. In the case of the Georgia Hotel Tax exemption form, it's about verifying a government official's or employee's eligibility for tax exemption. The W-9, on the other hand, is used to confirm someone's taxpayer identification number for income reporting, but both require specific information to ensure the correct tax treatment.

Non-Profit Organization Tax Exemption Certificate: Non-profit organizations often use a form to certify their tax-exempt status when purchasing goods or services to avoid paying sales tax. This parallels the Georgia Hotel Tax Form in that both certify an entity's eligibility for tax exemption. The crucial aspect is the official certification, without which tax would be applicable on purchases or services utilized.

Business License Registration Form: Although primarily used for the registration of a business entity within a locality, this form shares the commonality of requiring detailed information about an entity for governmental purposes. Both forms facilitate the verification of an entity's claims, whether for exemption from taxes or for the legitimate operation of a business within a specific jurisdiction.

Application for Government Grant: This form also collects detailed information about an entity or individual to verify eligibility, similar to the hotel tax exemption. It requires strict adherence to guidelines and accurate representation of eligibility to qualify for government funding, mirroring the process by which officials are exempted from hotel taxes under specific conditions.

Employee Travel Reimbursement Form: While serving a different purpose by dealing with post-travel claims, this document is related in focusing on the official business travels of employees or officers. It requires detailed accounting of expenditures during travel, similar to how the hotel tax form necessitates the identification and business purpose verification of a traveler to qualify for tax exemption.

Dos and Don'ts

When filling out the Georgia Hotel Tax form, it's important to follow guidelines to ensure the exemption process is carried out correctly. Here are five key actions to take, as well as five actions to avoid:

Do:

Verify the identity of the government official or employee using appropriate identification to ensure legitimacy.

Ensure that all payment methods for the lodging match the provided documentation, whether personal or government payment.

Provide and collect the State of Georgia Certificate of Exemption of Local Hotel/Motel Excise Tax form from the traveler.

Maintain a copy of the exemption form with hotel tax records to document the individual’s status and official business travel.

Contact the traveler’s accounting or fiscal office if there are any questions about the exemption process or required forms.

Don't:

Charge county or municipal excise tax on lodging to state or local government officials or employees traveling on official business.

Forget to require and retain a completed copy of the exemption form as part of your tax records.

Overlook the need to verify the official business of the traveler as stated on the certification section of the form.

Ignore the importance of confirming the acceptable payment methods, including personal or government payments.

Assume that the form is complete without checking for the signature of the official or employee, dates of lodging, and relevant government agency information.

Misconceptions

Navigating through the complexities of tax exemptions, especially for Georgia hotel operators, involves understanding the particulars of the Georgia Hotel Tax Form. From misconceptions about who qualifies for exemptions to what documentation is necessary, it's crucial to clear up common misunderstandings. Here are ten misconceptions about the Georgia Hotel Tax form and the realities behind them:

- Only state officials are exempt: A common misconception is that the exemption only applies to state officials. In reality, both state and local government officials or employees traveling on official business qualify for the exemption.

- All hotel taxes are exempted: Some believe that filling out the form exempts individuals from all hotel taxes. However, it specifically exempts them from county or municipal lodging excise taxes, not necessarily from other charges hotels might impose.

- No documentation is needed: Another misunderstanding is the belief that government officials don’t need to provide any documentation. In fact, they must provide a completed State of GA Certificate of Exemption of Local Hotel/Motel Excise Tax and, for sales tax exemption, a “Department of Revenue Sales Tax Certificate of Exemption Form (ST-5)”.

- Exemption applies to all forms of lodging: The exemption specifically applies to lodgings that are subject to local hotel/motel excise taxes. This doesn't automatically include all forms of overnight accommodations, like short-term rentals that might not be classified as hotels or motels.

- Payment method doesn’t matter: The exemption does indeed specify acceptable payment methods. For the excise tax, all forms of payment are accepted, but for the sales tax exemption, payment must be via a state of Georgia issued credit card or direct billing to the government organization.

- Only individuals on government business are exempt: While it's true that the individual must be traveling on official business, the form also requires the identification of a government agency and a contact within its accounting or fiscal office, indicating a broader verification process.

- The form is complicated to fill out: Some operators might think the form is complex and time-consuming. However, it simply requires basic information about the official or employee, their government agency, contact information, and the dates of lodging.

- Exemptions are automatically granted: Completion and submission of the form don’t automatically grant exemption. Verification of the individual’s government official or employee status is required, and hotels should keep a copy for their records.

- There’s no need to keep records: Contrarily, hotels must maintain copies of the exemption forms to document each individual’s status and the exemption’s validity, ensuring compliance with state regulations.

- Any government official traveling for any reason qualifies: It's imperative to understand that the exemption is only for those traveling on official government business. Personal trips, even by government officials or employees, do not qualify for the tax exemption.

For Georgia hotel and motel operators, being well-informed about these misconceptions and their clarifications ensures compliance with state laws and the proper administration of tax exemptions. Always refer to the latest guidelines and reach out to the proper fiscal contacts with any questions or uncertainties.

Key takeaways

Understanding the Georgia Hotel Tax Form is crucial for hotel and motel operators within the state to ensure proper tax exemption procedures are followed for eligible government officials and employees traveling on official business. Here are key takeaways:

- Effective April 2, 1987, Georgia state or local government officials or employees on official business are exempt from county or municipal hotel/motel excise taxes.

- To qualify for this exemption, the individual’s identity and official status must be verified by the hotel or motel operator.

- All payment methods, including personal or government payments, are accepted for the occupancy tax exemption.

- The State of GA Certificate of Exemption of Local Hotel/Motel Excise Tax form is required to grant this tax exemption.

- Operators must maintain a copy of this exemption form along with their hotel tax records as documentation of the individual’s eligibility.

- Inquiries regarding the exemption should be directed to the accounting or fiscal office contact provided by the traveler.

- The form includes sections for certification by the government official or employee, detailing the necessity of lodging for official duties and qualifying for tax exemption.

- Government officials or employees are also exempt from Georgia State Sales Tax if they submit the “Department of Revenue Sales Tax Certificate of Exemption Form (ST-5)” along with payment via a State of Georgia issued credit card or direct billing to the governmental organization.

- Understanding and accurately applying these exemptions can help avoid unnecessary tax charges and ensure compliance with Georgia law.

It’s essential for hotel and motel operators in Georgia to familiarize themselves with these requirements to streamline the process of accommodating government officials and employees while adhering to state tax exemption laws.

Popular PDF Forms

Georgia Att 15 - There are sections to disclose any direct or indirect interest in any alcoholic beverage business.

Georgia Notification - Facilitate a seamless asbestos project initiation in Georgia by ensuring the notification form is meticulously filled.

Mv-16 - Facilitates a smooth documentation process for purchase packages by providing a comprehensive checklist of acquisition costs.