Free Georgia St 5 Template in PDF

In the dynamic economic landscape of Georgia, the ST-5 form emerges as a pivotal document, sanctioned by the State's Department of Revenue, which grants purchasers the privilege to buy goods and services without bearing the burden of sales tax, under specific conditions. This Sales Tax Certificate of Exemption is especially crucial for entities engaging in transactions that demand tax-free or tax-exempt treatment, outlined distinctly across various categories in the form. The spectrum of eligibility spans from purchases made for resale, by government bodies, educational institutions like the University System of Georgia, to those made by specific authorities providing essential public services such as water or sewer service. Interestingly, the form also encompasses exemptions for tangible personal property intended for shipment or sale packaging and certain transportation equipment manufactured within the state for exclusive use outside. Unique provisions apply to aircraft, watercraft, and vehicles crossing state borders in commercial transport, and even to transactions involving the Federal Reserve Bank and credit unions. This document, underpinned by the Georgia Code and federal law references, embodies a detailed declaration by the purchaser, emphasizing the legal obligation to adhere strictly to the specified use of purchased goods and services to maintain the tax-exempt status. The intrinsic significance of the ST-5 form lies in its role as a testament to the purchaser's right to exemption while underlining the responsibilities that come with such exemptions, making it a subject of substantial interest for businesses and organizations navigating the complexities of tax regulations in Georgia.

Form Sample

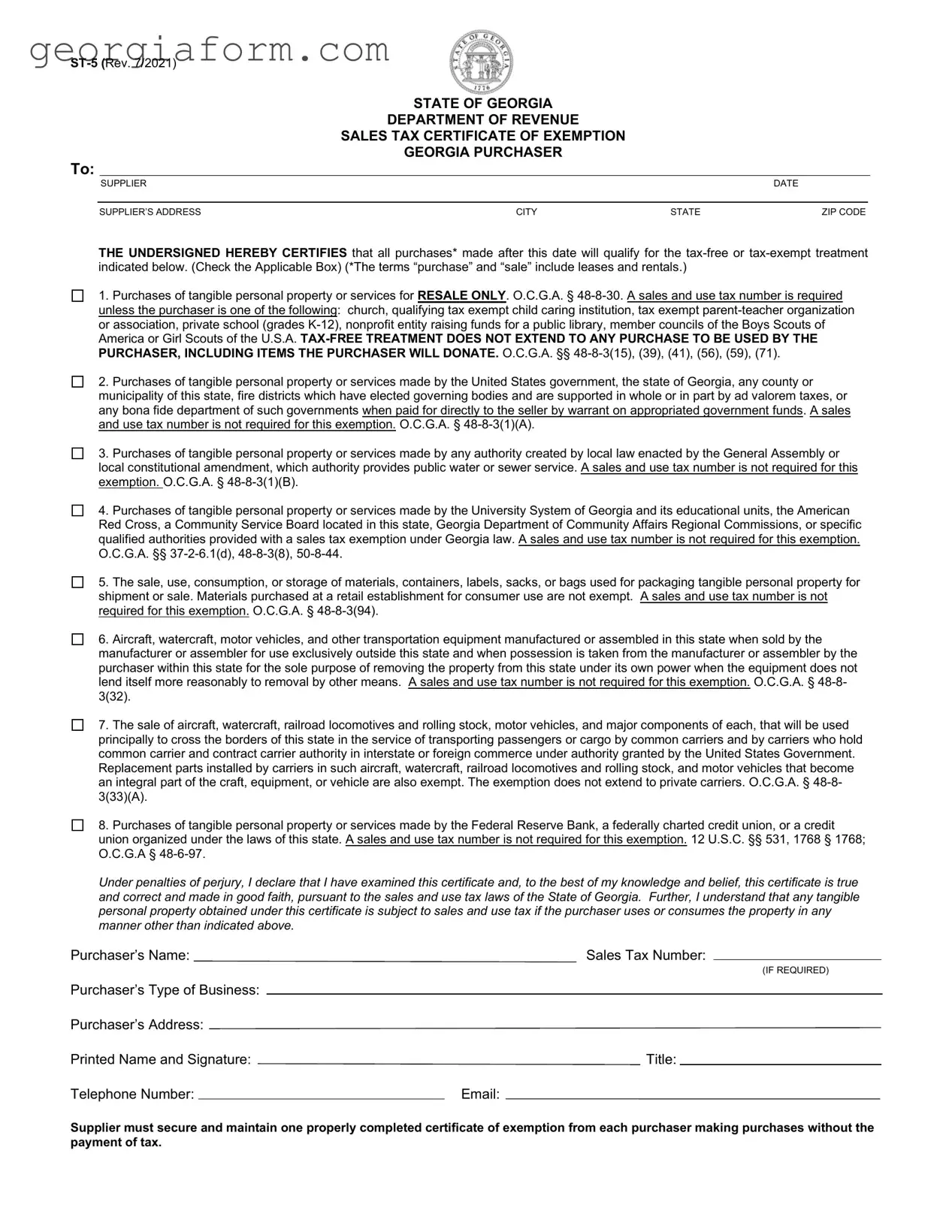

STATE OF GEORGIA

DEPARTMENT OF REVENUE

SALES TAX CERTIFICATE OF EXEMPTION

GEORGIA PURCHASER

To:

|

SUPPLIER |

|

|

DATE |

|

|

|

|

|

|

|

SUPPLIER’S ADDRESS |

CITY |

STATE |

ZIP CODE |

||

THE UNDERSIGNED HEREBY CERTIFIES that all purchases* made after this date will qualify for the

1. Purchases of tangible personal property or services for RESALE ONLY. O.C.G.A. §

2. Purchases of tangible personal property or services made by the United States government, the state of Georgia, any county or municipality of this state, fire districts which have elected governing bodies and are supported in whole or in part by ad valorem taxes, or any bona fide department of such governments when paid for directly to the seller by warrant on appropriated government funds. A sales and use tax number is not required for this exemption. O.C.G.A. §

3. Purchases of tangible personal property or services made by any authority created by local law enacted by the General Assembly or local constitutional amendment, which authority provides public water or sewer service. A sales and use tax number is not required for this exemption. O.C.G.A. §

4. Purchases of tangible personal property or services made by the University System of Georgia and its educational units, the American Red Cross, a Community Service Board located in this state, Georgia Department of Community Affairs Regional Commissions, or specific qualified authorities provided with a sales tax exemption under Georgia law. A sales and use tax number is not required for this exemption. O.C.G.A. §§

5. The sale, use, consumption, or storage of materials, containers, labels, sacks, or bags used for packaging tangible personal property for shipment or sale. Materials purchased at a retail establishment for consumer use are not exempt. A sales and use tax number is not required for this exemption. O.C.G.A. §

6. Aircraft, watercraft, motor vehicles, and other transportation equipment manufactured or assembled in this state when sold by the manufacturer or assembler for use exclusively outside this state and when possession is taken from the manufacturer or assembler by the purchaser within this state for the sole purpose of removing the property from this state under its own power when the equipment does not lend itself more reasonably to removal by other means. A sales and use tax number is not required for this exemption. O.C.G.A. §

7. The sale of aircraft, watercraft, railroad locomotives and rolling stock, motor vehicles, and major components of each, that will be used principally to cross the borders of this state in the service of transporting passengers or cargo by common carriers and by carriers who hold common carrier and contract carrier authority in interstate or foreign commerce under authority granted by the United States Government. Replacement parts installed by carriers in such aircraft, watercraft, railroad locomotives and rolling stock, and motor vehicles that become an integral part of the craft, equipment, or vehicle are also exempt. The exemption does not extend to private carriers. O.C.G.A. §

8. Purchases of tangible personal property or services made by the Federal Reserve Bank, a federally charted credit union, or a credit union organized under the laws of this state. A sales and use tax number is not required for this exemption. 12 U.S.C. §§ 531, 1768 § 1768; O.C.G.A §

Under penalties of perjury, I declare that I have examined this certificate and, to the best of my knowledge and belief, this certificate is true and correct and made in good faith, pursuant to the sales and use tax laws of the State of Georgia. Further, I understand that any tangible personal property obtained under this certificate is subject to sales and use tax if the purchaser uses or consumes the property in any manner other than indicated above.

Purchaser’s Name: |

Sales Tax Number: |

|

|||

|

|

|

|

|

(IF REQUIRED) |

Purchaser’s Type of Business: |

|

|

|

|

|

|

|

|

|

||

Purchaser’s Address: |

|

|

|

||

Printed Name and Signature: |

Title: |

|

|||

Telephone Number: |

|

|

Email: |

||

Supplier must secure and maintain one properly completed certificate of exemption from each purchaser making purchases without the payment of tax.

File Overview

| Fact Name | Detail |

|---|---|

| Purpose of Form ST-5 | This form certifies that the purchases made by the holder will qualify for tax-free or tax-exempt treatment under specific conditions outlined by the Georgia Department of Revenue. |

| Required Information | Purchasers must provide details including their name, type of business, sales tax number (if required), address, and contact information to complete the form. |

| Governing Law for the Exemptions | Several Georgia laws (O.C.G.A. §§) govern the tax exemptions available under this certificate, detailing specific conditions under which various items and services may be exempt from sales tax. |

| Exemption Criteria | The certificate covers a range of exemptions from sales tax for tangible personal property or services, including those made by government entities, certain nonprofit organizations, and for specific uses like resale or manufacturing for use outside the state. |

Guide to Using Georgia St 5

Filling out the Georgia ST-5 Form, which is a Sales Tax Certificate of Exemption, is an important process for businesses or entities that qualify for sales tax exemptions on purchases in Georgia. This document helps ensure that no sales tax is charged on qualifying purchases, which can include everything from tangible personal property to certain services. It's a straightforward form, but accuracy is crucial to avoid any complications or denials of exemptions. Below, you'll find a step-by-step guide to fill out the form correctly.

- Gather the necessary information before you start. This includes the sales tax number (if required), purchaser's type of business, address, and contact information.

- Enter the date at the top of the form. This indicates when the exemption certification becomes effective.

- Fill in the Supplier's Information, including the supplier's name, address, city, state, and zip code. This is who you are purchasing from.

- Under the section titled "The undersigned hereby certifies that all purchases made after this date will qualify for the tax-free or tax-exempt treatment indicated below," check the applicable box that corresponds to the reason for your tax-exempt purchase. Read each option carefully to ensure you choose the correct exemption category.

- In the section requesting the Purchaser’s Information, enter the:

- Purchaser’s Name,

- Sales Tax Number (if applicable - some exemptions do not require a sales tax number),

- Type of Business,

- Address (including city, state, and zip code),

- Printed Name and Signature of the person filling out the form,

- Title,

- Telephone Number, and

- Email address.

- Review all the information entered to ensure accuracy and completeness. Remember, providing false information can lead to penalties under perjury laws.

- Finally, submit the completed form to your supplier. They are required to retain a copy for their records to verify the tax exemption.

After successfully filling out and submitting the ST-5 form, your purchases from the supplier should not include sales tax, provided they fall within the exemption category you selected. It's a good idea to keep a copy of the completed form for your records and to note the expiration date, if any, of your exemption status. Should your exemption status change or the form expire, you'll need to submit a new ST-5 form to continue receiving tax-exempt purchases.

Obtain Clarifications on Georgia St 5

- What is the Georgia ST-5 form? The Georgia ST-5 form is a Sales Tax Certificate of Exemption issued by the State of Georgia Department of Revenue. It certifies that certain purchases made by the holder qualify for tax-exempt or tax-free treatment under specific conditions outlined by the state law.

- Who can use the Georgia ST-5 form? Entities such as churches, tax-exempt organizations like child caring institutions, parent-teacher organizations, private schools (K-12), nonprofits supporting public libraries, Scouts of America councils, government bodies, public water or sewer services authorities, educational units under the University System of Georgia, the American Red Cross, and certain transportation equipment manufacturers can use the ST-5 form. Federally chartered credit unions and those organized under state laws are also eligible.

- Do all purchasers need a Sales and Use Tax Number to use the ST-5 form? No, not all purchasers need a Sales and Use Tax Number to use the ST-5 form. Specific exemptions are provided where this number is not required, such as purchases made by government bodies, educational units, and certain tax-exempt organizations.

- Can the ST-5 form be used for personal purchases? No, the ST-5 form cannot be used for personal purchases or for items that the purchaser intends to use rather than resell. The tax-free treatment is specifically for items intended for resale, or for eligible entities’ use in their exempt functions and services.

- What types of purchases qualify for exemption using the ST-5 form? Qualifying purchases include tangible personal property or services for resale, purchases made directly by government bodies or specific exempt entities, materials used for packaging products for shipment or sale, certain transportation equipment, and other specific items detailed in the form's instructions.

- Is it necessary to fill out a new ST-5 form for every purchase? Not necessarily. Suppliers must maintain a completed ST-5 form on file for each exempt purchaser. As long as the form is valid, and the purchases fit the declared exempt purposes, a new form for each transaction is not required.

- What happens if a purchaser uses items obtained with the ST-5 form differently than stated? If items purchased under the ST-5 form are used in a manner other than what is indicated for exemption, the purchaser is then subject to pay sales and use tax on those items. Misuse of the exemption can result in penalties.

- How do I declare that the information on the ST-5 form is correct? The purchaser must sign the ST-5 form, declaring under penalty of perjury that the information provided is true, correct, and made in good faith in accordance with the sales and use tax laws of the State of Georgia. This includes accurate representation of the purchaser’s eligibility and intended use of the exempt purchases.

Common mistakes

When filling out the Georgia ST-5 Form, which is the Sales Tax Certificate of Exemption, there are common mistakes that can lead to incorrect filing, potential fines, or misuse of the form. Being aware of these mistakes can ensure that individuals and organizations use the exemption correctly and remain compliant with Georgia tax laws.

Not checking the correct exemption box or failing to understand the specific exemption criteria. Each exemption has specific requirements outlined by the Georgia Department of Revenue, and it's crucial to select the exemption that accurately reflects the purpose of the purchases.

Entering an incorrect sales tax number or leaving it blank when required. Certain exemptions still require the purchaser to provide a valid sales and use tax number unless the purchase falls under specific categories, such as purchases by churches or government entities that are exempt by law.

Misinterpreting the exemption for resale. The form explicitly states that tax-free treatment does not extend to any purchase to be used by the purchaser, including items that will be donated. Misuse of this exemption can lead to penalties.

Failing to provide accurate or complete information about the purchaser’s type of business, which helps in the validation process of the exemption claim.

Omitting the purchaser's address or providing an incorrect address, which is necessary for documentation and potential audits.

Not including a printed name and signature alongside the title, telephone number, and email. This information is critical for verification and contact purposes regarding the exemption certificate.

Assuming that all purchases made under the exemption certificate are automatically exempt without considering the use or consumption of the purchased property. If the property is used or consumed in a manner different than what is allowed under the exemption, it becomes subject to sales and use tax.

Forgetting to update or renew the exemption certificate when necessary. Exemption certificates do not last indefinitely and must be kept current to avoid misuse and remain in compliance.

To avoid these mistakes, it's vital to thoroughly review the ST-5 form instructions, verify all information before submission, and consult with a tax professional or the Georgia Department of Revenue if there are any questions regarding the proper use of the exemption.

Documents used along the form

When working with the Georgia ST-5 Sales Tax Certificate of Exemption, several other forms and documents might be used in conjunction to ensure that businesses and organizations comply with state tax regulations. These additional forms serve various purposes, from reporting sales tax collected to documenting tax-exempt purchases. Understanding each document's purpose can help streamline tax-related processes.

- ST-1 Sales and Use Tax Return: This form is essential for businesses required to report and remit the sales tax they have collected. While the ST-5 form is about tax exemption, the ST-1 form ensures that any sales tax due from non-exempt transactions is properly reported and paid to the state.

- ST-3 Sales and Use Tax Report: Used by businesses to detail the sales, purchases, and exchanges of tangible personal property. It's crucial for companies that have both tax-exempt and taxable transactions, helping them keep detailed records as required by law.

- ST-12 Resale Certificate for Sales Tax: This certificate is used by businesses when purchasing items they intend to resell. Similar to the ST-5, this certificate allows businesses to purchase inventory without paying sales tax at the point of sale. The exemption is based on the premise that sales tax will be collected when the items are sold to the end customer.

- ST-4 Sales Tax Certificate of Exemption for Resale and Nonprofit Organizations: Like the ST-5, this certificate is issued to qualifying nonprofit organizations and entities purchasing goods for resale. It specifies the conditions under which purchased goods are exempt from sales tax, providing a broader scope than the ST-5 in terms of the types of entities that can use the certificate.

These documents together play a significant role in the administration of sales and use tax in Georgia. Proper use and management of these forms can help businesses and organizations ensure compliance with tax laws, avoid penalties, and streamline their operations related to tax reporting and exemption claims.

Similar forms

The Uniform Sales & Use Tax Exemption/Resale Certificate – Multijurisdiction form shares similarities with the Georgia ST-5 form in that both serve the purpose of exempting the holder from sales tax on purchases intended for resale, or that qualify under specific tax-exempt purposes. However, the multijurisdiction form is used for transactions across multiple states, not just within Georgia.

The Florida Consumer's Certificate of Exemption (Form DR-14) is akin to the ST-5 form as both certify that an entity is exempt from paying state sales tax on eligible purchases. The basis for exemption may vary, but the principle behind both forms is to document tax-exempt status.

The California Resale Certificate (Form BOE-230) is used much like the ST-5 form to allow businesses to purchase goods tax-free, provided those goods are intended for resale. Both serve as declarations to suppliers about the purchaser's right to a tax exemption.

Similarly, the Illinois Certificate of Resale (Form CRT-61) functions like the Georgia ST-5 form, granting businesses the ability to buy products without paying sales tax if those products are to be resold. The key aspect here is the intent to resell the purchased goods, which exempts the transaction from sales tax in both states.

The New York Resale Certificate (Form ST-120) is comparable to the ST-5 form because it is given to sellers to document the intent of purchasing goods for resale, exempting such transactions from sales tax. Both certificates are critical for tax compliance in their respective states.

The Texas Sales and Use Tax Exemption Certification (Form 01-339) shares the goal of the ST-5 form by certifying that an organization or business is eligible to purchase items tax-free for specific exempt purposes, like resale, similar to the criteria set forth in Georgia's ST-5 form.

Michigan Sales and Use Tax Certificate of Exemption (Form 3372) resembles the ST-5 form in that it allows businesses and organizations to document their eligibility for exemption from sales tax. While each state has unique conditions and uses for their exemption forms, the underlying concept remains constant.

The North Carolina Sales and Use Tax Agreement Certificate of Exemption (Form E-595E) is used to certify tax-exempt purchases, paralleling the ST-5 form's purpose for entities in Georgia claiming sales tax exemptions on eligible transactions.

The Oregon Business Registry Resale Certificate, though Oregon does not have a state sales tax, serves a similar function for Oregon businesses purchasing goods out of state that they intend to resell. It identifies the purchaser as a reseller, preventing sales tax from being charged in states with reciprocal tax exemption agreements.

Lastly, the Colorado Multi-jurisdiction Sales Tax Exemption Certificate functions in a manner similar to the ST-5 by exempting the holder from sales tax on qualifying purchases. It is particularly used for transactions that span across jurisdictions, providing flexibility for businesses operating in multiple states.

Dos and Don'ts

When filling out the Georgia ST-5 form, a Sales Tax Certificate of Exemption, it's crucial to adhere to guidelines to ensure the process is complete, accurate, and compliant with state laws. Below are lists of things you should and shouldn't do while filling out this form.

Do:

- Review the form carefully to understand the types of exemptions available and determine which one applies to your purchase.

- Include your sales tax number if required by the specific exemption you're claiming. Certain exemptions do not require this number, but many do.

- Clearly print or type the name of the purchaser, type of business, address, and contact information to ensure legibility and accuracy.

- Check the appropriate box to indicate the tax-free or tax-exempt treatment that applies to your purchases.

- Sign and date the form to certify that the information provided is correct and made in good faith.

- Retain a copy of the completed form for your records as proof of exemption.

- Ensure that the supplier’s address, city, state, and ZIP code are filled out correctly to avoid processing delays.

- Review the penalties for perjury statement to understand the legal implications of providing false information.

- Communicate with your supplier to confirm they have received and accepted your ST-5 form.

Don't:

- Leave any required fields blank. Incomplete forms could be rejected or cause delays in processing.

- Assume all purchases are exempt without checking the specific conditions for tax-free treatment listed in the instructions.

- Use the form to claim exemptions not explicitly covered by the checkboxes or without proper justification under Georgia law.

- Forget to specify the purchaser’s type of business; this information is essential for validating the exemption eligibility.

- Submit the form without the purchaser’s signature and title. An unsigned form is not valid.

- Ignore the date field. The exemption is only valid for purchases made after the date indicated on the form.

- Misinterpret the exemption categories. Each category has specific qualifications that must be met.

- Assume a sales tax number is not required without confirming. Check each exemption’s requirements carefully.

- Overlook updating the form if any relevant business or contact information changes after submission.

Misconceptions

Understanding the Georgia State Form ST-5, the Sales Tax Certificate of Exemption, can be somewhat complex, leading to various misconceptions. It's crucial to clarify these misunderstandings to ensure compliance and the correct application of exemptions. Here are nine common misconceptions:

- Any purchase is tax-exempt if you have an ST-5 form: The ST-5 exemption specifically applies to purchases outlined in the form, such as tangible personal property or services for resale, or purchases by specific entities like governments or certain non-profits. It doesn’t cover all purchases.

- All non-profit organizations are eligible for an ST-5 exemption: Only those non-profits that meet Georgia’s criteria, such as schools, churches, and certain charitable organizations, can use the ST-5 to make tax-exempt purchases.

- The form grants indefinite tax-exempt status: The ST-5 form must be updated periodically. It serves as a declaration for a specific period; thus, entities must ensure their eligibility and compliance are continuously maintained.

- A sales tax number is always required: While many entities must provide a sales tax number when using the ST-5, there are exceptions. Government entities, for instance, do not need one for their exemptions.

- The exemption applies to all kinds of sales, including services: The ST-5 primarily exempts tangible personal property or certain services mentioned within the form from the sales tax. Not every service an organization purchases is exempt.

- There is no need to maintain records if you have an ST-5: Suppliers must secure and retain a properly completed ST-5 form for each exempt transaction. This documentation is vital for audits or reviews by tax authorities.

- Once completed, the ST-5 automatically applies to all future purchases: The purchaser must certify that all future purchases after the date of the form will qualify for tax-exempt treatment based on the conditions stated in the ST-5. It doesn’t automatically apply without this certification for every transaction.

- You can use the ST-5 for personal purchases if you're part of a qualifying organization: The ST-5 is strictly for purchases made for the organization's use. Personal purchases, even if made by someone within a qualifying organization, are not covered by the exemption.

- Any violation of the ST-5 terms is inconsequential: Misuse of the ST-5, such as claiming exemption for non-qualifying purchases, can lead to penalties, fines, and revocation of tax-exempt status. It’s imperative to understand and adhere to the form’s conditions.

Correctly applying the ST-5 exemptions impacts both the purchaser’s and the supplier’s compliance with Georgia’s tax laws. It’s essential for eligible organizations to thoroughly understand the form's stipulations and limitations to maintain their exemptions and avoid penalties.

Key takeaways

When dealing with the Georgia ST-5 Sales Tax Certificate of Exemption, it's important to grasp its purpose and how to correctly fill it out and use it. Here are four key takeaways to guide you through this process:

- Understand the exemption categories: The ST-5 form outlines specific types of purchases that qualify for sales tax exemption. These include purchases of tangible personal property or services for resale, by certain government entities, authorities providing public services, the University System of Georgia and its units, and specific types of equipment and transportation. Each category has its own criteria and requirements that must be met to qualify for the exemption.

- Know when a sales tax number is required: While many of the exemptions do not require a sales tax number, certain categories, like purchases for resale, necessitate a valid sales and use tax number unless the purchaser falls into specific exempt groups (e.g., churches, certain nonprofits). It's crucial to check whether your purchase falls into a category that requires a sales tax number.

- Ensure proper use of obtained items: Items bought under a tax exemption certificate must be used in the manner stated on the form. Any deviation, such as using the items for personal use or outside the specified exemption parameters, subjects them to sales and use tax. Misuse of exempt purchases can lead to penalties.

- Maintaining accurate records: Suppliers are required to secure and maintain a properly completed exemption certificate from each purchaser claiming a sales tax exemption. This documentation is crucial for both parties to verify that the exemption was properly claimed and to safeguard against potential audits or disputes.

By keeping these takeaways in mind, you can ensure that your use of the Georgia ST-5 form is compliant and beneficial for your tax exemption needs.

Popular PDF Forms

Free Purchase Agreement Form - The form addresses legal issues such as title authority, easements, boundary disputes, and zoning violations, requiring sellers to disclose any known issues.

Ga Workers Compensation - Facilitates communication between injured workers, employers, insurers, and the State Board on the status and specifics of a claim.