Legal Promissory Note Form for Georgia

In the realm of finance and personal lending in Georgia, the promissory note holds significant value as an instrument of commitment. This document, acting as a formal pledge, delineates the terms under which money is borrowed and the manner in which it will be repaid. It's of paramount importance for both lenders and borrowers to understand the content and implications of this form. Within its framework, the Georgia Promissory Note form encompasses several key components, including but not limited to the amount of the loan, interest rates applied, repayment schedule, and the consequences of non-payment. By meticulously outlining these details, the form does not only provide a clear roadmap of the financial transaction but also serves as a legal tool for ensuring accountability and safeguarding the interests of both parties involved. As such, navigating through its clauses and specifications with a comprehensive understanding is crucial for a smooth lending process and the prevention of possible disputes.

Form Sample

Georgia Promissory Note Template

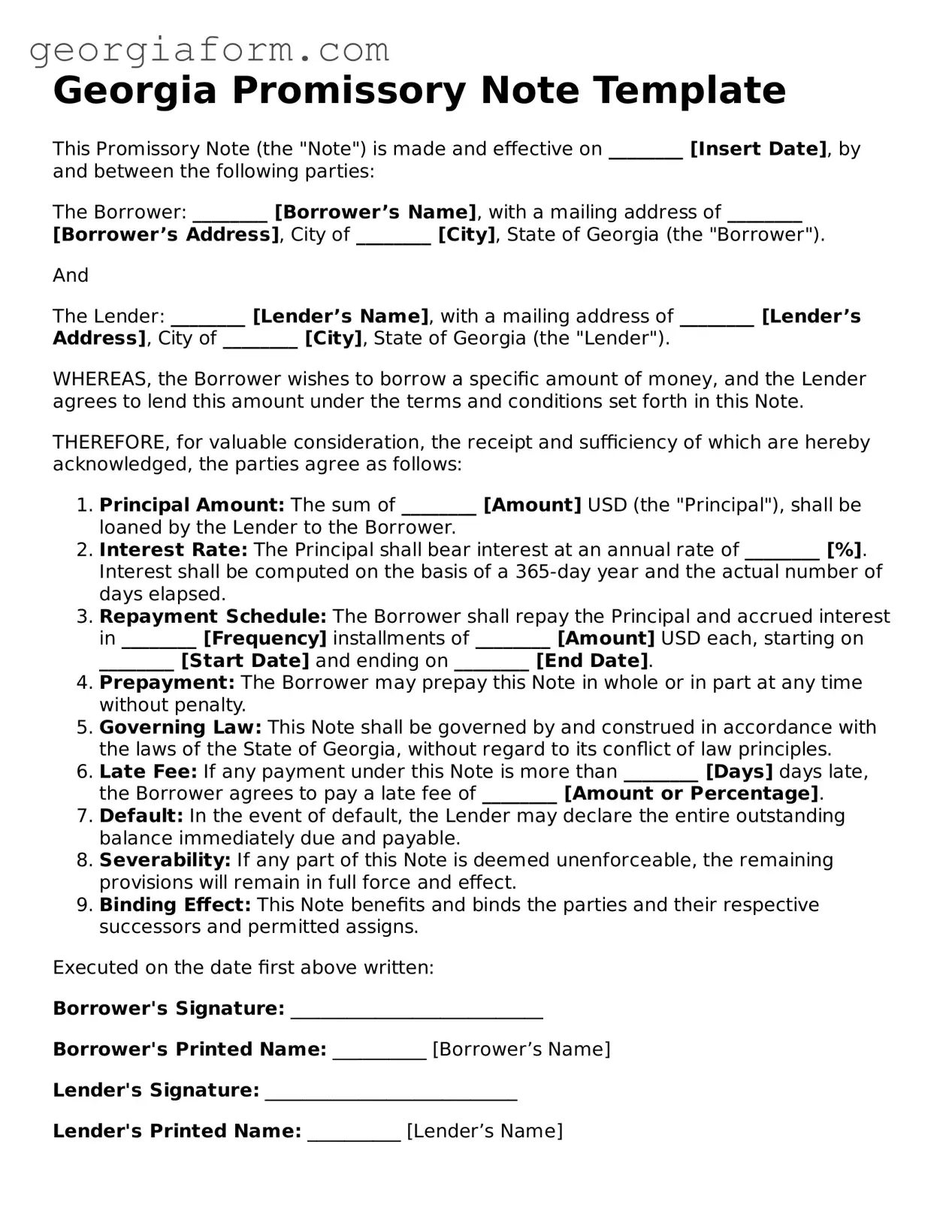

This Promissory Note (the "Note") is made and effective on ________ [Insert Date], by and between the following parties:

The Borrower: ________ [Borrower’s Name], with a mailing address of ________ [Borrower’s Address], City of ________ [City], State of Georgia (the "Borrower").

And

The Lender: ________ [Lender’s Name], with a mailing address of ________ [Lender’s Address], City of ________ [City], State of Georgia (the "Lender").

WHEREAS, the Borrower wishes to borrow a specific amount of money, and the Lender agrees to lend this amount under the terms and conditions set forth in this Note.

THEREFORE, for valuable consideration, the receipt and sufficiency of which are hereby acknowledged, the parties agree as follows:

- Principal Amount: The sum of ________ [Amount] USD (the "Principal"), shall be loaned by the Lender to the Borrower.

- Interest Rate: The Principal shall bear interest at an annual rate of ________ [%]. Interest shall be computed on the basis of a 365-day year and the actual number of days elapsed.

- Repayment Schedule: The Borrower shall repay the Principal and accrued interest in ________ [Frequency] installments of ________ [Amount] USD each, starting on ________ [Start Date] and ending on ________ [End Date].

- Prepayment: The Borrower may prepay this Note in whole or in part at any time without penalty.

- Governing Law: This Note shall be governed by and construed in accordance with the laws of the State of Georgia, without regard to its conflict of law principles.

- Late Fee: If any payment under this Note is more than ________ [Days] days late, the Borrower agrees to pay a late fee of ________ [Amount or Percentage].

- Default: In the event of default, the Lender may declare the entire outstanding balance immediately due and payable.

- Severability: If any part of this Note is deemed unenforceable, the remaining provisions will remain in full force and effect.

- Binding Effect: This Note benefits and binds the parties and their respective successors and permitted assigns.

Executed on the date first above written:

Borrower's Signature: ___________________________

Borrower's Printed Name: __________ [Borrower’s Name]

Lender's Signature: ___________________________

Lender's Printed Name: __________ [Lender’s Name]

PDF Data

| Fact Number | Description |

|---|---|

| 1 | The Georgia Promissory Note form is a legal document that outlines a loan's terms, conditions, and repayment details between two parties. |

| 2 | This form serves as a written promise from the borrower to repay the lender a specific amount of money by a certain date. |

| 3 | Georgia's Promissory Notes can be either secured or unsecured, indicating whether the loan is backed by collateral. |

| 4 | The Governing Law for the Georgia Promissory Note form is the State of Georgia's legal code, ensuring compliance with state-specific legal standards and requirements. |

| 5 | Interest rates on loans outlined in the Promissory Notes must adhere to the legal limits set by Georgia law to avoid being deemed usurious. |

| 6 | In the event of a dispute, details within the Promissory Note form can be used in court to uphold the agreement. |

| 7 | The form must be signed by both the borrower and the lender, making it a legally binding agreement. |

| 8 | Details such as payment schedule, interest rate, amount borrowed, and the names of the parties involved must be clearly stated in the form. |

Guide to Using Georgia Promissory Note

Filling out a Georgia Promissory Note is a straightforward process that legally documents the agreement between two parties regarding the borrowing of money. This document serves as a commitment by the borrower to pay back the lender under the terms outlined in the note. It is crucial that both the lender and borrower understand the terms and conditions set forth to ensure compliance and avoid potential disputes. The following steps will guide you through completing the Georgia Promissory Note form accurately.

- Start by entering the date the promissory note is being created at the top of the form.

- Write the full legal names of the borrower and the lender in the designated spaces.

- Specify the principal loan amount in dollars.

- Detail the interest rate per annum that will apply to the principal amount.

- Outline the repayment schedule including the start date, the number of payments, the frequency of payments (e.g., monthly), and the amount of each payment.

- If applicable, describe any collateral that the borrower has agreed to secure the loan with.

- Include provisions for late fees and what constitutes a default on the loan.

- Specify any co-signer’s information, if a co-signer is part of the agreement, including their full legal name and relationship to the borrower.

- Both the borrower and the lender must sign and date the form, acknowledging their understanding and agreement to the terms.

- Notarization: While not always mandatory, having the signatures notarized can add an additional layer of legal protection.

Upon completion, it is important for both parties to keep copies of the signed promissory note. This document serves as a legal record of the loan and can be used to resolve disputes or misunderstandings regarding the repayment terms.

Obtain Clarifications on Georgia Promissory Note

-

What is a Georgia Promissory Note?

A Georgia Promissory Note is a legal document where a borrower promises to repay a loan to a lender according to agreed-upon terms. This document includes the total amount of money borrowed, the interest rate (if applicable), repayment schedule, and the consequences of non-payment. In Georgia, as in other states, this note serves as a binding agreement and can be secured, meaning backed with collateral, or unsecured, depending on the agreement between the parties involved.

-

How is a Promissory Note Different from a Loan Agreement in Georgia?

While a promissory note and a loan agreement might seem similar, they serve different purposes and contain varying levels of detail. A promissory note is a straightforward agreement that outlines the basics of the loan and the repayment promise. Conversely, a loan agreement is more comprehensive and includes additional clauses related to borrower and lender obligations, representations, warranties, and covenants. In short, a promissory note is a simple promise to pay, whereas a loan agreement creates a broader contractual relationship.

-

Are Promissory Notes Legally Enforceable in Georgia?

Yes, promissory notes are legally enforceable in Georgia. For a promissory note to be enforceable, it must include specific information such as the amount of money loaned, the repayment schedule, and the signatures of the involved parties. Additionally, for the document to hold up in court, it must be clear that both parties intended to enter into a binding agreement. It's advisable to have a witness or notary public sign the note to add an extra layer of verification and enforceability.

-

What Should You Include in a Promissory Note in Georgia?

- The full names and contact information of the lender and borrower.

- The principal amount of the loan.

- The interest rate, if applicable, and how it is calculated.

- The repayment schedule including dates and amounts.

- Any collateral securing the loan, if it is a secured promissory note.

- The signatures of both parties and, ideally, a witness or notary public.

- Any specific clauses related to late payment penalties or what happens in case of default.

While this list covers the basics, it's crucial to ensure that the promissory note complies with Georgia law and accurately reflects the agreement between the lender and borrower. Professional legal advice can help tailor the document to the specific situation.

Common mistakes

When filling out the Georgia Promissory Note form, several common errors can lead to complications or misunderstandings down the line. Being aware of these mistakes can help ensure that the document is completed correctly.

Not specifying the exact amount loaned in clear figures. It's essential to state the loan amount both in numerals and words to avoid any confusion.

Omitting the interest rate. In Georgia, failing to include the interest rate could default the loan to the state's legal interest rate, potentially not what the parties intended.

Forgetting to define the repayment schedule. A clear repayment schedule, including the frequency of payments and their due dates, is crucial.

Not clarifying the collateral, if any. If the loan is secured, describing the collateral ensures both parties understand what is at stake.

Leaving out terms regarding late fees or missed payments. Specifying these terms upfront can prevent disputes later.

Failing to include a clause about prepayment. Whether prepayment is allowed and if any penalties apply should be clearly indicated.

Skiping details about the parties involved. Full names and addresses of the borrower and lender ensure the agreement is enforceable.

Omitting signatures and dates. These are essential for the note's legality and enforceability.

Ignoring governing law. Stating that Georgia law governs the note helps in resolving any legal issues under the state's jurisdiction.

Using ambiguous language. Clear and precise terms prevent misunderstandings and legal issues.

Understanding and addressing these mistakes can help both the borrower and lender create a promissory note that accurately reflects their agreement and protects their interests.

Documents used along the form

In the realm of financial agreements, especially those involving personal loans in Georgia, the promissory note stands out for its clarity and legal binding. This document spells out the repayment terms, interest rates, and other critical conditions between a borrower and a lender. However, to ensure the integrity of the transaction and to safeguard the interests of both parties, a promissory note is often accompanied by other legal documents. Understanding these supporting documents can provide a more secure and comprehensive approach to personal lending.

- Loan Agreement: This document complements a promissory note by providing detailed terms and conditions of the loan. While the promissory note acknowledges the debt and the repayment plan, the loan agreement may include clauses on collateral, default conditions, and actions that can be taken in case of non-payment, making it more comprehensive.

- Security Agreement: If the loan is secured with collateral, a Security Agreement is essential. It outlines the specific asset(s) pledged as security by the borrower to ensure loan repayment. This agreement gives the lender a lien on the collateral, permitting seizure if the borrower defaults, thus reducing the lender’s risk.

- Guaranty: To further protect the interests of the lender, a guaranty can be used. This document involves a third party, the guarantor, who agrees to fulfill the repayment obligations should the borrower fail to do so. It provides an additional layer of security for the loan.

- Amortization Schedule: Often used alongside a promissory note, an Amortization Schedule offers a breakdown of each payment over the course of the loan term. It details how payments are split between principal and interest, helping both borrower and lender track the balance and interest over time.

While the promissory note itself is a crucial document for any loan transaction, these additional documents help to clarify, secure, and manage the loan more effectively. For anyone engaging in lending or borrowing, especially with significant amounts or over long periods, taking the time to understand and prepare these supplementary documents can prevent misunderstandings and legal complications, ultimately ensuring a smoother and more transparent transaction.

Similar forms

A Mortgage Agreement is similar to a Promissory Note in that it is a binding document where a borrower agrees to pay back a lender per the terms specified. However, a Mortgage Agreement secures the loan with real property as collateral.

A Loan Agreement is akin to a Promissory Note, detailing the loan's terms, interest rate, repayment schedule, and the obligations of the borrower. The distinction often lies in the complexity; loan agreements are generally more detailed and involve larger sums.

The IOU (I Owe You) document share similarities with a Promissory Note, as both outline an amount owed by one party to another. The major difference is the level of formality and detail; an IOU is more informal and usually lacks specifics on repayment terms and interest.

A Personal Guarantee ties closely to a Promissory Note as both commit the signer to fulfill certain financial obligations. In personal guarantees, an individual (or entity) promises to take responsibility for someone else's debt if they default on their agreement.

A Credit Agreement is like a Promissory Note in its function to detail the terms under which credit is extended from one party to another, including repayment schedule and interest rates. Credit agreements typically cover more extensive transactions and involve multiple parties.

The Bond is a form of investment that is similar to a Promissory Note but is used in public and corporate finance. A bond formalizes the borrower's promise to repay the principal along with interest at fixed intervals.

A Debt Settlement Agreement is related to a Promissory Note as it involves the repayment of borrowed money. However, it specifically refers to an agreement where the lender agrees to accept less than the amount owed as full payment.

A Secured Promissory Note is a direct variant of the standard Promissory Note, adding a layer of security for the lender by collateralizing an asset. If the borrower defaults, the lender has the right to seize the asset to cover the debt.

The Installment Agreement shares principles with a Promissory Note, especially in outlining a repayment structure. It differs in that it specifically establishes a series of regular payments over time until the debt is fully paid.

Dos and Don'ts

When filling out the Georgia Promissory Note form, understanding the dos and don'ts ensures that the agreement is legally binding, clear, and protects both the lender and the borrower. Below, you'll find essential guidelines compiled to help navigate the process effectively.

- Do ensure all parties are correctly identified. Include full legal names, addresses, and contact details of both the lender and the borrower to avoid any ambiguity regarding the identities of the involved parties.

- Do be clear about the loan amount and repayment terms. Specify the principal amount being loaned and the interest rate applied. Clearly outline the repayment schedule, including due dates and whether payments are monthly or at another agreed frequency.

- Do include the governing state law. Confirm that the note specifies Georgia law governs the agreement. This is crucial for ensuring that any future legal matters are handled under the appropriate jurisdiction.

- Don't neglect to specify the consequences of late payments or default. Clearly define any fees for late payments, the grace period (if any), and the steps that will be taken in the event of a default. This information helps prevent misunderstandings and provides a clear course of action if the terms are not met.

- Don't forget to have the document witnessed or notarized if required. Depending on the amount of the loan or the agreement between the parties, having the document witnessed or notarized can add an extra layer of legal protection and authenticity.

- Don't leave out any agreed-upon collateral. If the loan is to be secured with collateral, detail this arrangement in the promissory note. Describe the collateral and state the conditions under which the lender can seize it if the borrower fails to meet the payment terms.

Adhering to these guidelines will contribute to a well-prepared promissory note that protects all parties involved. It's essential to review the completed document carefully before signing to ensure that all the terms are correctly captured and agreed upon.

Misconceptions

Understanding the Georgia Promissory Note form is vital for anyone engaging in lending or borrowing money in Georgia. However, several misconceptions surround its use and legal standing. Clarifying these misconceptions ensures that individuals are better informed about their rights and obligations under this financial instrument.

- All promissory notes in Georgia are the same: This is a common misunderstanding. The reality is that promissory notes can vary widely in terms of interest rates, repayment schedules, and consequences of default. Customization is often necessary to reflect the specific terms agreed upon by the lender and borrower.

- A notary must witness the signing: While having a promissory note notarized can add a layer of formality and help in the enforcement of the document, Georgia law does not require notarization for a promissory note to be considered legal and binding. The critical requirement is the acknowledgment of the note by the borrower and lender.

- Verbal agreements can substitute for a promissory note: Relying on verbal agreements in financial transactions is risky and can lead to disputes that are difficult to resolve. A written promissory note provides a clear record of the terms agreed upon and is enforceable in a court of law, unlike most verbal agreements related to debts.

- A promissory note is only useful for loans between individuals: This is not the case. Businesses often use promissory notes for loans, sales of goods on credit, or other transactions requiring a promise of payment. They are versatile instruments used across various contexts, not limited to personal loans.

- If the borrower defaults, the lender must sue to recover the debt: While legal action is one route to recover a defaulted debt under a promissory note, it is not the only option. The parties can agree on alternative settlement methods or modifications to the payment terms to avoid court proceedings. Moreover, the note might include provisions that allow for other forms of recourse, such as repossession of collateral.

It is essential for both lenders and borrowers in Georgia to understand these nuances of promissory notes. This understanding not only helps in crafting a document that aligns with their needs but also in managing their expectations regarding the note's enforcement and legal significance.

Key takeaways

When engaging with the Georgia Promissory Note form, it is essential to grasp the fundamental principles governing its use and filling out process. This document serves as an official agreement between a borrower and a lender, detailing the loan and its repayment. The following takeaways offer guidance to ensure compliance and understanding of this binding financial instrument:

- Identification of Parties: Clearly state the full legal names, addresses, and contact information of the borrower and the lender. This identification establishes the accountability and the roles of each party involved.

- Loan Amount and Interest Rate: The principal amount being borrowed should be explicitly mentioned along with the interest rate agreed upon. Georgia law dictates the maximum interest rate allowed; this form must comply with these legal limits to avoid being deemed usurious.

- Repayment Schedule: Detail the terms of repayment, including the start date, frequency of payments (monthly, quarterly, etc.), and the duration of the loan. This schedule gives both the borrower and the lender a clear timeline of expectations.

- Late Fees and Penalties: Specify any applicable charges for late payments or missed payments to deter delinquency and to ensure both parties are aware of the consequences.

- Security or Collateral: If the promissory note is secured, describe the collateral that the borrower is offering to guarantee the loan. This description should be detailed enough to clearly identify the collateral without ambiguity.

- Governing Law: Indicate that the promissory note is governed by the laws of the State of Georgia. This ensures that any dispute resolution adheres to the local state laws, providing both parties with knowledge of their legal standing.

- Signatures: The document must be signed by both the borrower and the lender, and in some cases, a witness or notary public. These signatures legally bind the parties to the agreement as outlined in the promissory note.

- Prepayment: Address the terms of prepayment, if any, allowing the borrower to pay off the loan earlier than the agreed-upon schedule. This section should specify whether there is a penalty or not for early repayment.

Understanding these key aspects of the Georgia Promissory Note form can significantly affect its enforceability and the protection it offers both borrowers and lenders. Carefully preparing and reviewing all details in the note will help ensure that it meets all legal requirements and accurately reflects the agreement between the parties.

More Georgia Templates

Georgia Foreclosure - It is beneficial for borrowers facing financial difficulties, offering a dignified exit from their mortgage obligations.

How to Get Power of Attorney for Elderly Parent in Georgia - Residents of long-term care facilities may use a Power of Attorney to appoint someone to handle their financial and healthcare decisions.