Free Sf 16 Georgia Template in PDF

The SF 16 Georgia form plays a crucial role for participants in the Georgia Dream Homeownership Program, outlining the steps to accurately determine the acquisition cost of a home and its surrounding land. This form is essential when submitting a purchase package exclusively for the Georgia Dream First Mortgage Program. It meticulously guides both the borrower and the property seller through calculating the total cost, including the price paid for the residence and any related fixtures or land, interest during construction (if applicable), and various settlement and financing costs. Extraordinary specifics like the appraised value of gifted land and the capitalization of ground rent for leasehold mortgages are also accounted for, ensuring a comprehensive evaluation. Not only does this form subtract the value of personal property and services rendered by the borrower or their family, which may offset the mortgage loan amount, but it also affirms the livability standard of the sold land. Accurate completion and submission of the SF 16 Georgia form, under the penalty of perjury, are vital for the proper function and integrity of the home buying process, underscoring its importance in maintaining clarity and honesty within Georgia's affordable housing initiatives.

Form Sample

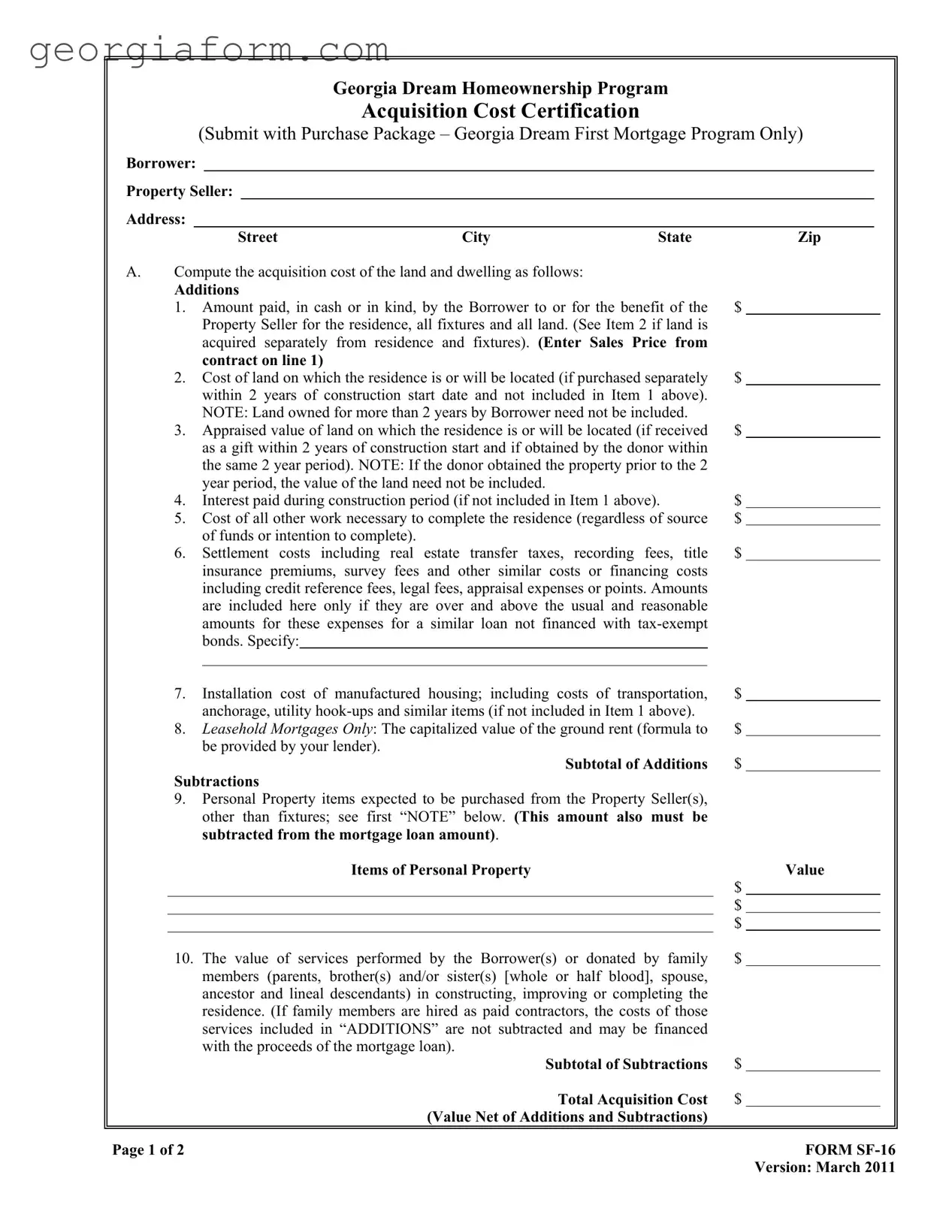

Georgia Dream Homeownership Program

Acquisition Cost Certification

(Submit with Purchase Package – Georgia Dream First Mortgage Program Only)

Borrower:

Property Seller:

Address:

Street |

City |

State |

Zip |

A.Compute the acquisition cost of the land and dwelling as follows:

Additions |

|

|

1. |

Amount paid, in cash or in kind, by the Borrower to or for the benefit of the |

$ |

|

Property Seller for the residence, all fixtures and all land. (See Item 2 if land is |

|

|

acquired separately from residence and fixtures). (Enter Sales Price from |

|

|

contract on line 1) |

|

2. |

Cost of land on which the residence is or will be located (if purchased separately |

$ |

|

within 2 years of construction start date and not included in Item 1 above). |

|

|

NOTE: Land owned for more than 2 years by Borrower need not be included. |

|

3. |

Appraised value of land on which the residence is or will be located (if received |

$ |

|

as a gift within 2 years of construction start and if obtained by the donor within |

|

|

the same 2 year period). NOTE: If the donor obtained the property prior to the 2 |

|

|

year period, the value of the land need not be included. |

|

4. |

Interest paid during construction period (if not included in Item 1 above). |

$ |

5. |

Cost of all other work necessary to complete the residence (regardless of source |

$ |

|

of funds or intention to complete). |

|

6. |

Settlement costs including real estate transfer taxes, recording fees, title |

$ |

|

insurance premiums, survey fees and other similar costs or financing costs |

|

including credit reference fees, legal fees, appraisal expenses or points. Amounts are included here only if they are over and above the usual and reasonable amounts for these expenses for a similar loan not financed with

7. |

Installation cost of manufactured housing; including costs of transportation, |

$ |

|

anchorage, utility |

|

8. |

Leasehold Mortgages Only: The capitalized value of the ground rent (formula to |

$ |

|

be provided by your lender). |

|

|

Subtotal of Additions |

$ |

Subtractions

9.Personal Property items expected to be purchased from the Property Seller(s), other than fixtures; see first “NOTE” below. (This amount also must be subtracted from the mortgage loan amount).

Items of Personal Property

$

$

$

Value

|

10. The value of services performed by the Borrower(s) or donated by family |

$ |

|

|

|

|

members (parents, brother(s) and/or sister(s) [whole or half blood], spouse, |

|

|

|

|

|

ancestor and lineal descendants) in constructing, improving or completing the |

|

|

|

|

|

residence. (If family members are hired as paid contractors, the costs of those |

|

|

|

|

|

services included in “ADDITIONS” are not subtracted and may be financed |

|

|

|

|

|

with the proceeds of the mortgage loan). |

|

|

|

|

|

Subtotal of Subtractions |

$ |

|

|

|

|

Total Acquisition Cost |

$ |

|

|

|

|

(Value Net of Additions and Subtractions) |

|

|

|

|

|

|

|

|

||

|

Page 1 of 2 |

|

FORM |

||

|

|

|

Version: March 2011 |

||

NOTE: A “fixture” is property that is affixed to real estate, which the Borrower(s) intend(s) (i): to keep so affixed during its useful life, and (ii) to be part of the real estate. Refrigerators,

NOTE: The acquisition cost of a Single Family Dwelling does not include:

(1)Usual and reasonable settlement and financing costs; “Settlement Costs” include titling and transfer costs, title insurance, survey fees and other similar costs; and “Financing Costs” include credit reference fees, legal fees, appraisal expenses, points which are paid by the Borrower, or other costs of financing the residence. Such amounts must not exceed the usual and reasonable costs which otherwise would be paid for in a similar loan,

(2)The imputed value of services performed by the Borrower or members of his family (which include only the Borrower’s parents, brother(s) and/or sister(s) [whether by whole or half blood], spouse, ancestors and lineal descendant(s) in constructing or completing the residence, or

(3)The cost of land which has been owned by the Borrower for at least 2 years before the date on which the construction of the structure comprising the Single Family Residence begins.

B.To the best of our knowledge, all of the land sold with this residence reasonably maintains the basic livability of the residence.

I fully understand the information set forth above is material to the Georgia Department of Community Affairs and declare under penalty of perjury, which is a felony offense in the State of Georgia that the above information is true and correct.

Subject Property Address: ________________________________________________________________

__________________________________________________________________ , Georgia

Borrower’s Signature |

|

Date |

|

|

|

|

Date |

|

|

|

|

Property Seller’s Signature |

|

Date |

|

|

|

Property Seller’s Signature |

|

Date |

I further certify that the real estate on which the home is located does not provide a source of income to the borrower.

______________________________________________________ |

________________________________ |

Borrower’s Signature |

Date |

______________________________________________________ |

________________________________ |

Co Borrower’s Signature |

Date |

Page 2 of 2 |

FORM |

|

Version: March 2011 |

File Overview

| Fact | Detail |

|---|---|

| Form Name | Georgia Dream Homeownership Program Acquisition Cost Certification |

| Purpose | To certify the acquisition cost of a property within the Georgia Dream First Mortgage Program |

| Applicants | Borrowers purchasing a property under the Georgia Dream Homeownership Program |

| Included Information | Costs associated with the purchase including land and dwelling, construction interest, settlement costs, and any deductions for personal property or donated services. |

| Exclusions | Personal property not affixed to the real estate, customary financing and settlement costs, and land owned by the borrower for more than 2 years prior to construction. |

| Legal Requirement | Submission is required with the Purchase Package for Georgia Dream First Mortgage Program eligibility. |

| Governing Law | Overseen by the Georgia Department of Community Affairs, adhering to state-specific guidelines and requirements. |

| Verification Statement | Borrowers declare under penalty of perjury that all provided information is true and correct. |

| Income Source Certification | Borrowers must certify that the real estate on which the home is located does not provide a source of income. |

Guide to Using Sf 16 Georgia

When applying for the Georgia Dream Homeownership Program using the SF-16 form, applicants focus on outlining the acquisition cost details of the property they wish to purchase. This form is essential for providing a detailed financial snapshot concerning the property acquisition, which helps in determining eligibility and compliance with program requirements. Following the correct steps ensures accurate submission, which is key in the application process.

- Start with the section titled "Borrower" by entering the full name of the person or people applying for the loan.

- In "Property Seller," write the full name of the individual or entity selling the property.

- Under "Address," input the street, city, state, and zip code of the property involved in the transaction.

- Move to section A, titled "Compute the acquisition cost of the land and dwelling as follows." Begin by adding the sales price of the residence along with all fixtures and land in item 1. This value should come directly from the sales contract.

- If the land was purchased separately within two years prior to the start of construction and not included in item 1, write down the cost of this land in item 2.

- For land received as a gift within two years of the construction start, whose donor obtained it within that same timeframe, enter its appraised value in item 3.

- Include the interest paid during the construction period in item 4, if it's not already accounted for in item 1.

- Item 5 requires the cost of all other work necessary to complete the residence. Include all relevant expenses, regardless of the funding source or completion intention.

- Specify and sum up settlement and financing costs over and above usual amounts for a similar loan financed without tax-exempt bonds in item 6.

- For Item 7, if applicable, enter the installation cost of manufactured housing, including transportation and utility hook-ups.

- In item 8, note the capitalized value of the ground rent for leasehold mortgages only.

- Next, move to the subtractions section and deduct any personal property items purchased from the seller that are not considered fixtures in item 9.

- Subtract the value of services performed by the Borrower(s) or donated by family members in item 10.

- Calculate and enter the "Subtotal of Additions" and "Subtotal of Subtractions," then compute the "Total Acquisition Cost" which is the value net of additions and subtractions.

- Proceed to certify the information by writing the subject property address on the indicated line.

- The borrower and co-borrower (if applicable) must sign and date the form, along with the property seller who also needs to provide their signature and date.

- Lastly, the borrower and co-borrower must certify that the property does not provide a source of income to them by signing and dating in the space provided.

Once every step is correctly followed, and the form is filled out completely, applicants can submit their SF-16 form as part of their purchase package for the Georgia Dream First Mortgage Program. It is crucial to ensure all information is accurate and true to avoid any legal repercussions or delays in the application process.

Obtain Clarifications on Sf 16 Georgia

What is the SF-16 Georgia form used for?

The SF-16 Georgia form, known as the Georgia Dream Homeownership Program Acquisition Cost Certification, is a critical document in the purchase process for those participating in the Georgia Dream First Mortgage Program. This form helps in calculating the total acquisition cost of a home, including both the land and dwelling. It accounts for various expenses such as the sales price, cost of land if bought separately, interest during construction, and settlement costs among others. It's essential for ensuring that the purchase meets the program's guidelines.

Who needs to fill out the SF-16 form?

The form must be completed by the borrower participating in the Georgia Dream Homeownership Program. Additionally, the property seller must also provide information and signatures to verify the sale's details. This form is submitted with the purchase package, making it a joint responsibility of both the borrower and the seller.

Which expenses are included in the acquisition cost according to the SF-16 form?

- Price paid for residence and land

- Cost of land if purchased separately within a specific timeframe

- Appraised value of land if received as a gift

- Interest paid during the construction period

- Cost of work necessary to complete the residence

- Settlement and financing costs exceeding usual amounts

- Installation cost for manufactured housing

- Capitalized value of ground rent for leasehold mortgages

This comprehensive list ensures accurate representation of the property's total cost.

What items are subtracted from the total acquisition cost?

- Value of personal property items to be purchased separately from fixtures

- Imputed value of services performed by the borrower or family members in constructing or improving the residence

These subtractions prevent the double-counting of values and ensure the acquisition cost reflects only the property itself and related improvements.

How does one calculate the total acquisition cost using the SF-16 form?

The total acquisition cost is calculated by adding the various expenditures related to acquiring the property and then subtracting certain values, such as personal property purchases and imputed value of services by the borrower or family members. It provides a net value that reflects the true cost of acquiring the property under the program's guidelines.

Why must the borrower declare the information under penalty of perjury?

Accuracy and honesty in declaring acquisition costs are paramount to the integrity of the Georgia Dream Homeownership Program. By requiring a declaration under penalty of perjury, the program emphasizes the seriousness of providing truthful and accurate information. This legal stance helps prevent fraud and ensures that only eligible applicants benefit from the program.

Can the cost of land owned for more than two years be included in the acquisition cost?

No, the cost of land that has been owned by the borrower for at least two years before the construction start date of the residence is not included in the total acquisition cost. This provision distinguishes between recent property transactions relevant to the current purchasing process and property that has been held as a long-term asset.

Common mistakes

When individuals embark on the journey of filling out the SF 16 Georgia form for the first time, which is essential for the Georgia Dream Homeownership Program, a series of common mistakes often arise. Paying close attention to these errors can substantially streamline the application process, ensuring that applicants stay on the right path towards securing their dream home. The list below outlines eight frequent missteps:

- Failing to accurately capture all components of the acquisition cost, including both the cash transactions and in-kind contributions made towards the purchase. This oversight can lead to underreporting the total investment, which is a critical figure for the program.

- Omitting the cost of land acquired separately from the dwelling, especially if this purchase happened within two years prior to the start of the construction. This detail is vital for an accurate calculation of the total acquisition price.

- Misunderstanding the conditions under which the appraised value of gifted land should be included. If the land was received as a gift within two years of the construction start date and was acquired by the donor within the same timeframe, its value must be factored into the total acquisition cost.

- Excluding interest paid during the construction period from the calculations, assuming it falls outside the scope of initial costs. This interest is a direct component of the acquisition cost if not already included in the sales price.

- Overlooking the additional expenses necessary to complete the residence, including funds from sources other than the buyer or those tied to future improvement plans. All such expenses contribute to the final acquisition cost.

- Incorrectly including usual and reasonable settlement and financing costs in the total acquisition cost. These costs, although significant, are separately accounted for and should not inflate the purchase price calculated for the program.

- Overcomplicating the subtraction of personal property items expected to be purchased from the Property Seller, which are not considered part of the acquisition cost but must be deducted from the mortgage loan amount. Identifying these items correctly ensures the accuracy of both the acquisition cost and mortgage calculations.

- Incorrectly adding or forgetting to subtract the value of services performed by the borrower or donated by family members from the total acquisition cost. If these services are contracted and paid for, they are not subtracted but rather included in the additions.

Understanding these common pitfalls can greatly assist applicants in accurately completing the SF 16 Georgia form. A careful and thorough review of all entries will help in preventing these mistakes, ultimately facilitating a smoother journey towards homeownership under the Georgia Dream program.

Documents used along the form

When processing the SF-16 Georgia form for the Georgia Dream Homeownership Program, several additional documents and forms are often required to complete the purchase package. These documents ensure that all aspects of the home purchase are accurately documented and in compliance with applicable regulations. Understanding these forms can help streamline the home buying process.

- Loan Application Form: This form captures the borrower's financial information, employment history, and details about the property being purchased. It is used by lenders to assess the borrower's creditworthiness and ability to repay the loan.

- Home Appraisal Report: An appraisal report provides an expert opinion on the value of the property being purchased. It includes an analysis of comparable sales in the area and an assessment of the property's condition. This report ensures that the loan amount does not exceed the property’s value.

- Proof of Homeowners Insurance: This document verifies that the borrower has obtained insurance coverage for the property. Lenders require homeowners insurance to protect their investment in case of damage or loss.

- Closing Disclosure: The Closing Disclosure is a detailed statement of the final loan terms and closing costs. Borrowers receive this document at least three business days before closing on the mortgage. It allows them to review the details of the loan and compare them with the Loan Estimate issued at the beginning of the application process.

Together with the SF-16 Georgia form, these documents form a comprehensive package that supports the financing of a home through the Georgia Dream Homeownership Program. Preparing these documents in advance can help ensure a smooth and efficient home buying process.

Similar forms

The HUD-1 Settlement Statement: Similar to the SF 16 Georgia form, the HUD-1 Settlement Statement details the financial transactions involved in a real estate purchase. It itemizes all charges imposed on buyers and sellers in connection with the sale, including the acquisition cost, settlement costs, and adjustments. The SF 16 form also focuses on the calculation of acquisition costs, including settlement and financing costs, which parallels the comprehensive financial breakdown provided by the HUD-1.

Uniform Residential Loan Application (URLA): The URLA is used to apply for a mortgage and includes information about the borrower, the property, and the requested loan. Its similarity to the SF 16 form lies in the requirement to provide detailed property information and the emphasis on the borrower's acknowledgment and certification of the details provided, a feature shared with the SF 16's borrower declarations and certifications.

Good Faith Estimate (GFE): Before it was replaced by the Loan Estimate, the GFE provided borrowers with an estimate of their loan costs and settlement charges. Like the SF 16 form, it detailed expected costs involved in acquiring a property, including settlement costs and any other fees related to the mortgage transaction. Both documents are designed to give a detailed financial overview to help borrowers understand their financial obligations.

Real Estate Settlement Procedures Act (RESPA) Disclosures: RESPA requires that borrowers receive disclosures at various times in the transaction process. The SF 16 form shares the intent of RESPA disclosures by ensuring borrowers are fully informed about the costs of their real estate transaction, specifically the acquisition costs, which include details on settlement costs and adjustments.

Truth in Lending Act (TILA) Disclosure: TILA disclosures provide borrowers with information about the costs of their credit, including the annual percentage rate (APR), finance charge, amount financed, and payment schedule. The SF 16 form complements this by detailing the acquisition costs and adjustments, offering a clear picture of the financial aspects of purchasing a property, albeit focused on the property and construction specifics.

Construction Loan Agreement: This document outlines the terms, conditions, and disbursement schedule of a loan taken out to construct a residence. The SF 16 form is similar in that it includes costs related to the construction or completion of a residence, such as interest during construction, and outlines the total acquisition cost involving land and dwelling, which are key figures in construction loan agreements.

Appraisal Report: Appraisals are key in real estate transactions to determine the property's market value. The SF 16 form requires the appraised value of land if it is received as a gift, directly relating to the property's valuation as provided in an appraisal report. Both documents serve to establish value, but the SF 16 form uses this information in calculating the acquisition cost, combining valuation with the financial specifics of the purchase.

Dos and Don'ts

When completing the SF-16 Georgia form for the Georgia Dream Homeownership Program, it's crucial to navigate the process correctly to ensure that your application is successful. Here are the things you should and shouldn't do:

Things You Should Do

Ensure all the information provided is accurate and true. Double-check the details of the acquisition cost, including sales price, cost of land, and settlement costs, to avoid any inaccuracies that could lead to legal issues.

Include all necessary costs in the Additions section, such as the cost of land (if purchased separately), interest paid during construction, and the installation cost of manufactured housing. Overlooking any relevant cost can affect the total acquisition cost calculation.

Specify and subtract any personal property items and the value of services performed by the borrower or donated by family members in the Subtractions section. This ensures that the final acquisition cost is calculated correctly.

Consult with a professional if you’re unsure about any aspect of the form. This could be a real estate attorney or financial advisor who understands the ins and outs of the Georgia Dream Homeownership Program.

Things You Shouldn't Do

Don't underestimate the importance of the notes provided in the form. These notes contain crucial information about what should and shouldn't be included in your calculations, like the distinction between fixtures and personal property.

Avoid leaving sections blank. If a section doesn’t apply to your situation, write “N/A” or “0,” depending on the context. This shows that you have acknowledged and considered each part of the form.

Don't sign the form without reviewing all the information thoroughly. The declaration under penalty of perjury at the end of the form isn’t just a formality; it's a legal acknowledgment that the information you've provided is correct.

Refrain from including usual and reasonable settlement and financing costs in the acquisition cost, as spelled out in the form. These include title insurance, survey fees, legal fees, and similar expenses that are typical for a similar loan not financed with tax-exempt bonds.

Misconceptions

Navigating the intricacies of homeownership forms can be a daunting task, and the SF-16 Georgia form, associated with the Georgia Dream Homeownership Program, is no exception. There are numerous misconceptions floating around. Let's demystify some of the most common misunderstandings to ensure buyers and sellers alike can proceed with confidence.

Misconception 1: The SF-16 form is only required for first-time homebuyers.

This is incorrect. While the Georgia Dream Homeownership Program is designed to help first-time buyers, the SF-16 form, which certifies acquisition costs, must be submitted by all participants in the Georgia Dream First Mortgage Program, regardless of first-time homebuyer status.

Misconception 2: Personal property included in the sale affects the total acquisition cost.

Actually, the value of personal property expected to be purchased from the seller, which is not considered a fixture to the real estate, should be subtracted from the acquisition cost on the SF-16 form. This reduction ensures that the calculation reflects the cost of the real estate only.

Misconception 3: The interest paid during the construction period is always part of the acquisition cost.

This is not always the case. If the interest paid during the construction period is already included in the initial sales price, it is not added again to the cost calculations on the SF-16 form.

Misconception 4: Settlement and financing costs are always included in the acquisition cost.

While some settlement and financing costs do get added to the acquisition cost, it is specified that only those over and above usual and reasonable amounts for a similar loan not financed with tax-exempt bonds are included. This dispels the idea that all such costs should be added indiscriminately.

Misconception 5: The value of land owned for more than two years before construction must be included.

On the contrary, the SF-16 form specifically states that the cost of land owned by the borrower for at least 2 years before the start of construction does not need to be included in the acquisition cost.

Misconception 6: The appraised value of land received as a gift should always be included.

The truth is, the appraised value of land received as a gift within 2 years of construction start and obtained by the donor within the same period should be included. If the donor acquired the land prior to this period, its value is not added to the total.

Misconception 7: Improvements made by family members are financed through the mortgage loan.

Incorrect. The SF-16 form guidance states that the value of services performed by family members in constructing or completing the residence should be subtracted from the acquisition cost, indicating that these contributions do not increase the loan amount.

Misconception 8: Leasehold mortgages are treated the same as other mortgages.

Leasehold mortgages have a specific consideration on the SF-16 form—the capitalized value of the ground rent, which is not a common factor in other types of mortgage calculations.

Misconception 9: All property that is affixed to real estate is considered a fixture.

There's a crucial clarification in the SF-16 form: certain items, despite being affixed to the property, like refrigerators and washers not built into the residence, are actually considered personal property, not fixtures.

Misconception 10: The calculation of total acquisition cost is straightforward.

The process involves several steps, including both additions and subtractions, to accurately determine the net value. Misunderstanding the items that need to be included or excluded can lead to errors in the final calculation, emphasizing the need for careful review and understanding of the form's instructions.

Understanding these misconceptions is vital for anyone involved in the Georgia Dream Homeownership Program. Armed with the correct information, applicants and real estate professionals can navigate the process more smoothly and with confidence.

Key takeaways

When filling out and using the SF-16 Georgia form, specifically designed for the Georgia Dream Homeownership Program, there are several key takeaways to keep in mind. This form is crucial for accurately reporting the acquisition cost related to purchasing a new home under this program, ensuring compliance with its guidelines and requirements.

- Comprehensive Cost Calculation: The form requires a detailed account of all costs involved in acquiring the property, including the purchase price, land cost if bought separately, appraised value of gifted land, and various construction and settlement costs. It is designed to capture the full financial picture of acquiring the home.

- Exclusions and Deductions: Certain costs are specifically excluded from the calculation of the total acquisition cost, such as personal property items not considered fixtures, the value of services performed by the borrower or family members, and land owned by the borrower for more than two years prior to construction. Understanding these exclusions is key to accurately reporting the total acquisition cost.

- Definition of Fixtures vs. Personal Property: The form distinguishes between fixtures, which are included in the acquisition cost, and personal property, which is not. Fixtures are items intended to be permanently attached to and part of the real estate, whereas personal property includes movable items not built into the residence.

- Settlement and Financing Costs: The form outlines that usual and reasonable settlement and financing costs do not count towards the acquisition cost calculation. However, if these costs are unusually high relative to similar loans not financed with tax-exempt bonds, they may need to be included.

- Accuracy and Honesty: By signing the form, borrowers and sellers declare under penalty of perjury that all information provided is accurate and truthful. This emphasizes the importance of carefully reviewing and ensuring all information is correct before submission.

- Income from Real Estate: Borrowers must certify that the real estate upon which the home is located does not provide a source of income to the borrower. This certification underscores the program’s focus on homeownership rather than income generation from property.

This form serves as a vital component of the purchase package for those participating in the Georgia Dream First Mortgage Program, ensuring that all parties have a clear understanding of the financial elements involved in the property acquisition.

Popular PDF Forms

Georgia Workers Compensation Forms - Filing this form is the first step in ensuring that injured workers receive necessary medical attention and financial support.

Workers Comp Insurance in Georgia - The requirement for physician approval within 60 days before the job offer underscores the emphasis on the employee's health and readiness for work.

Mortuary Schools in Georgia - Investigation into any past license sanctions, emphasizing the board's dedication to maintaining high standards.